Most counters in my watchlist are positive today as the STI gained to close just a whisker off 2,880. It would seem that the Chinese government has done the world a great favour by deciding to let the RMB strengthen. This is something I have believed should happen for some time. A stronger RMB would ameliorate the problem of inflation within China, raise the purchasing power of its people and improve standards of living. Increased domestic consumption would do a lot of good for China's own economy as well as the global economy. You might want to read what I wrote in an earlier post here.

STI +1.6%; More upside on window-dressing, says SIAS

Monday, 21 June 2010

Monday, 21 June 2010

© 2010 - The Edge Singapore

AIMS AMP Capital Industrial REIT: Volume expanded today and all trades were done at only one price, 22c. MACD has turned up. MACD histogram has a buy signal. MFI has turned up, forming a higher low. OBV has turned up, suggesting increased accumulation.

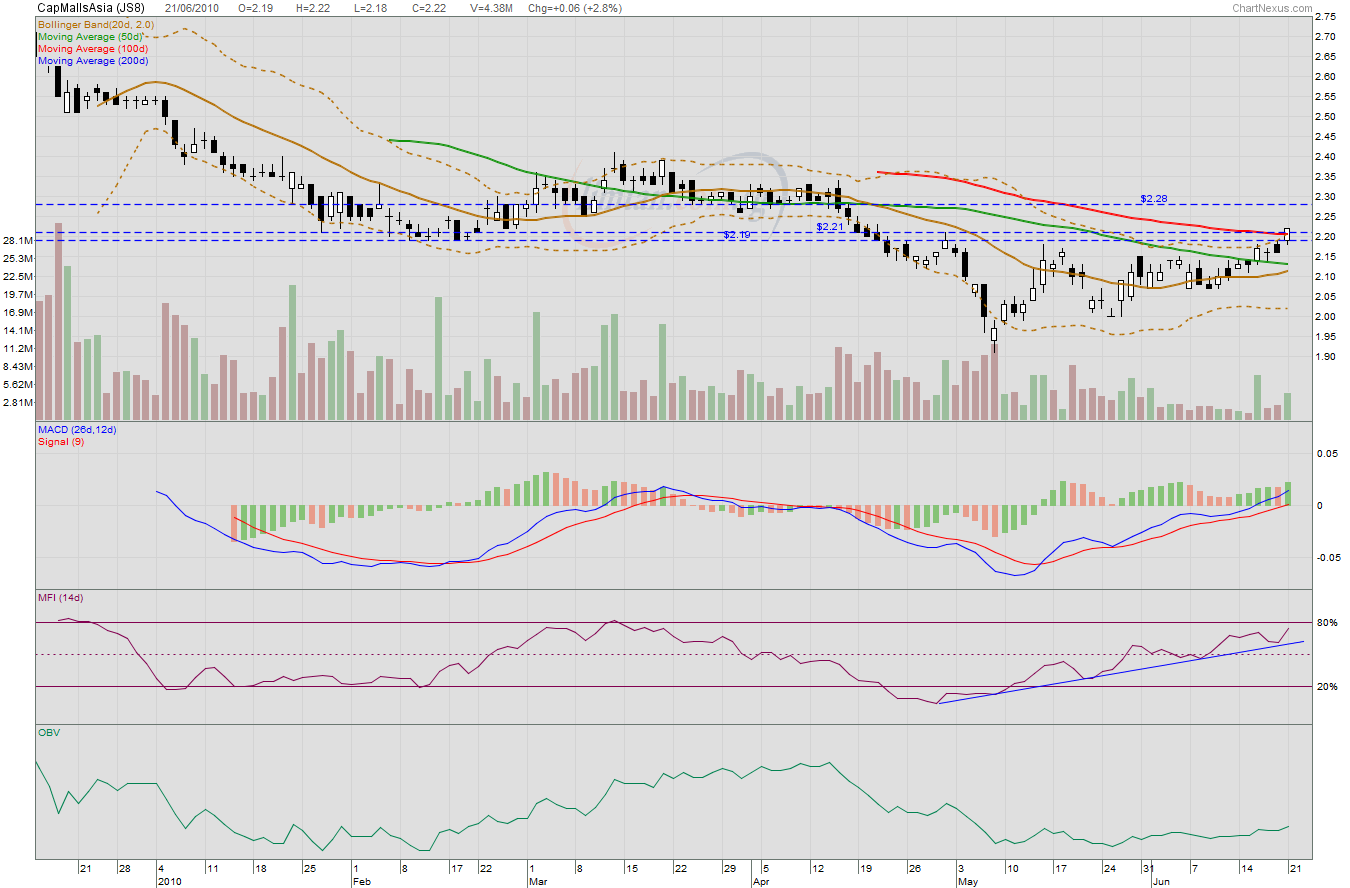

CapitaMalls Asia: Price broke the resistance band of $2.19 to $2.21 which I identified earlier. Closing at $2.22 seems bullish but volume suggests that this might not be durable. This counter is probably rising due to a lack of sellers rather than an abundance of buyers. Nonetheless, the momentum is still good as suggested by the MFI and price might be pushed higher.

Courage Marine: The picture is somewhat similar to CapitaMalls Asia. A white candle day on improved volume but not impressively so which suggests a lack of sellers rather than an abundance of buyers. MFI shows improving momentum while the OBV has turned up slightly. It remains to be seen if resistance at 20c could be taken out. A significant resistance after 20c is at 21c.

FSL Trust: MFI and OBV continue to rise. Could 40c be taken out this week? The next resistance level which is likely to be a strong one as suggested by candlesticks and a declining 20dMA is at 42c.

Golden Agriculture: Price continues to be resisted at 55c although it touched a high of 55.5c today. Momentum is still positive and MACD is about to cross into positive territory. Volume is, however, unimpressive which probably resulted in the failure to take out 55c and instead formed a white spinning top which is a possible reversal signal. Support is at 51.5c in case of a trend reversal.

LMIR: It seems that the merged 100d and 200d MAs are too strong to be taken out today. Price closed at 47.5c which is where we find the 50dMA, forming an inverted cross in the process. The negative divergence between price and volume continues to suggest LMIR has been rising on weak technicals. If the 50dMA does not hold up as support, the next support is at 46c as provided by the 20dMA.

Related posts:

AIMS AMP Capital Industrial REIT: Big boys.

Courage Marine: Triple bottom?

Golden Agriculture: Resistance remains at 55c.

LMIR: Testing resistance.

FSL Trust: Verona I.

Bloggy Award

Bloggy Award