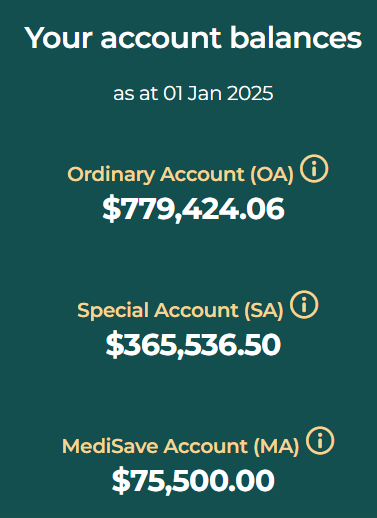

If you are part of my YouTube community, you might have seen the photos I shared on my latest CPF numbers.

Here they are for those who are not in the know,

I was fortunate that I was able to take advantage of higher yielding T-bills to grow my CPF savings at a faster clip in the last couple of years.

However, with the difference being very little in recent months, I have decided to simply leave the CPF OA money untouched for the time being.

I have just done a $4,000 Top Up to my CPF MA to hit the prevailing BHS in 2025.

Decided to do it now as January is going to be a busy month and I fear I might forget to do it later on.

Updated:

This Top Up will make 4% per annum risk free and will generate more interest income to pay for my medical insurance.

Of course, if we are still gainfully employed, doing this would also allow us to enjoy income tax relief.

We are fortunate to have the CPF system in Singapore.

We should take full advantage of our membership.

If AK can do it, so can you!

Published earlier in the day:

4Q 2024 passive income. Prep for 2025.

Bloggy Award

Bloggy Award

8 comments:

Did you ever use the SRS account?

Hi .

Yes, I did.

https://singaporeanstocksinvestor.blogspot.com/2024/02/srs-portfolio-in-2024-what-did-i-do.html?m=1

Hihi AK, I also topped up whatever I can for my own CPF which is just the MA. I also did 8k cash top-up for my parent's CPF RA to max out the tax reliefs. FYI, CPF has removed the age cap of 70 on the MRSS, and increased the annual matching grant to $2,000. So hit two birds with 1 stone. :)

Hi Yv,

That is good news for those who can benefit from MRSS. We are so lucky to have one of the best government regulated retirement funding systems in the world. 💯

Hi AK, thank you for your generous sharing. They are very inspiring.

Just to add on to your exchange with Yv on MRSS 2025. I did a quick search on CPF website (refer to link below) and it seems that the cash top up done for MRSS is not entitled for tax relief if I read it correctly?

https://www.cpf.gov.sg/service/article/from-2025-how-are-the-matching-grants-and-tax-relief-determined-for-my-cash-top-ups-made-to-a-senior-eligible-for-the-matched-retirement-savings-scheme

Hi Dan,

Thanks for sharing the link. 😊

Hi AK,

I have about $35k to max out my CPF MA as I have already max out my CPF SA,

Do you think is better to top up my MA yearly to $8k (for tax deduction) or just max out MA for higher interest?

(Assuming there is no SRS or other avenue for tax relief)

Can you talk to yourself?

Kamsiah...

Hi jasoho,

It would depend on which option gives you greater benefit.

Do you benefit more from the tax relief or from the interest earned from a larger lump sum contribution?

Post a Comment