The next speaker was Associate Professor Tan Ern Ser from the Department of Sociology in NUS. His presentation looked at three categories of seniors aged 55-65, 65-74 and those 75 and older.

In general, younger seniors as well as male seniors do better in having CPF savings. More older seniors receive retirement funding from their children compared to the younger seniors.

This, to me, shows that the CPF has become a more important part of retirement funding for Singaporeans and will continue to be so for younger generations, basic safety net though it may be.

Prof Tan also revealed that despite some worries, most of our seniors have seemingly been prudent with the CPF money they withdrew. See table below:

|

| Usage of withdrawn CPF money. |

Frankly, if I were to withdraw my CPF money just to plonk almost half of it in a savings account, I would rather leave it in the CPF to earn 4% per annum in interest.

Of course, this could change in future. Who knows? By the time I reach 55 years of age, fixed deposits in the banks here could attract interest payments of more than 5% per annum.

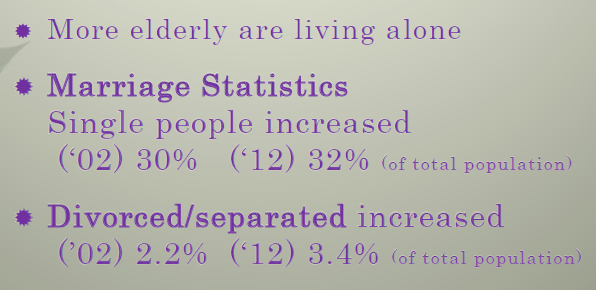

What I also found interesting is in the next slide:

Prof Tan asked whether good relationships with children lead to financial adequacy for the seniors or does financial adequacy of the seniors affect their relationships with their children?

Well, I think that if the reliance on children should be an important part of some people's retirement planning, then, this could be an interesting question to ponder.

OK, who threw a shoe at me? Who? Who?

See slides: here.

Related posts:

1. AK attended a forum on CPF.

2. What is our attitude towards having children?

Bloggy Award

Bloggy Award