One year ago, at a bit more than 49 years old, my CPF savings hit $1 million or a bit more.

It was a really good way to start the year in 2021.

This year is even better.

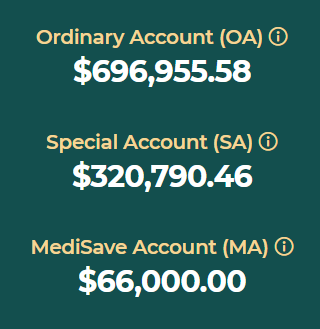

My CPF savings made a total of $31,207.95 in interest income in 2021.

Of course, recently, I made a Top Up to my MA as well as Voluntary Contributions to my OA and SA.

See:

2022 CPF Top Up and Voluntary Contribution done!

Now, if we put everything together, I have almost $1.1M in CPF savings!

So nice to start 2022 with an absolutely auspicious bang!

See:

I am staying the course and will continue to grow my CPF savings with some much appreciated help from the government.

As I am a retiree, I will have to grow my CPF savings voluntarily which is more demanding compared to people who are still in the workforce.

However, it is definitely worthwhile.

The volatility free and risk free nature of CPF coupled with attractive "coupons" makes it the ideal investment grade bond for me.

See:

Retire with an investment grade bond and an annuity.

The strategy really isn't difficult to understand.

However, I do understand that depending on our circumstances, we might not need to or be able to execute the strategy.

Of course, some might not even want to.

It doesn't really matter to me.

After all, ASSI is just a blog for me to talk to myself.

Eavesdrop if you like and if you like what you hear, good.

If the ideas work for you, even better.

Don't be like some people.

See:

Unhappy with CPF and angry with AK!

To everyone who is on the same rewarding CPF journey, congratulations!

Huat with CPF!

Really, time does fly.

Remember this blog from 2015?

AK is buying a 12 year tenor AAA bond.

Do the right thing.

Do it early.

Reminder:

Don't do silly things and we can retire smart too.

Of course, AK is just talking to himself again.

If you are new to ASSI, you might want to read the following blogs:

1. This guy has $800K in his CPF!

2. Investors eat crusty bread with ink slowly for peace of mind.

Bloggy Award

Bloggy Award

29 comments:

Congrats,AK! Definitely waiting for my own CPF to reach that figure in future. I think I should be able to MAX my SA and my BHS by end of the year or by jan/Feb 2023. One milestone to be checked off by then! Definitely hoping for 1M55!

Hi Chasingdreams,

Thanks! :D

No regrets making the CPF a cornerstone in my retirement funding plan. :)

Getting rich slow isn't a bad thing. ;p

Reference:

Building a cornerstone in retirement funding with CPF.

Congrats AK. My wife and my CPF is $1.47m generated $51k of interest and etc. I top up my wife's CPF to catch up as started working about 12 years ago

The power of compounding interests!!! Care to share the breakdown of your interest earn for all 3 accounts?

Hi Siew Mun,

Husband and wife CPF team!

Gong xi gong xi! :D

You are a good husband and a good father.

Gambatte! :D

Hi Unknown,

Alamak, have to log into CPF account to check again.

You can do an estimate from the funds I have in my OA, SA and MA.

AK lazy. ;p

Compound interest FTW! :D

Reference:

$1.5m in CPF savings by doing nothing henceforth.

Some readers might find this blog interesting:

Good men top up their wives' CPF accounts.

Hi AK! Do you consider to transfer some of your OA to SA? So much more you could get by just transferring.

Hi 摇木马的小孩,

Oh, I would do OA to SA transfer now if I could.

Unfortunately, once our SA has hit the prevailing FRS, OA to SA transfer is not allowed.

You might be interested in this blog:

4 ways to beef up our CPF savings.

I am targeting to hit that magic number $191k this year!!!! Then I can relax and let it compound on its own. :).

Hi TDT,

If my experience is anything to go by, your SA will be on auto-pilot from then on. :D

Reading comments like yours makes me happy. :)

Reminds me of blogs such as this:

Hit FRS in SA by age 32. Stunned!

Why do you top up to MA when any amounts here can’t be withdrawn?

Hi ak,

What happen if we have hit the retiresum and we cant top up anymore ?

Karen

Hi Unknown,

I have published my reply as a blog.

See:

Why Top Up my CPF Medisave Account?

Hi Karen,

I suppose you mean the SA having the Full Retirement Sum?

Yes, in this case, not allowed to Top Up the SA anymore.

If we have maxed out our CPF accounts, we must find other ways.

See:

CPF is all we need unless we are very rich.

Hi AK

Thank you for sharing your CPF journey.

I had also embarked on a similar and rewarding journey sometime back.

I used cash to pay for my properties.

I understand that after 55, we can just withdraw the interest earned, still leaving the principal sum in OA/SA/RA untouched.

But I would rather leave the interest there, unless I have better use for it, for example, use it to top up my dad’s RA (which will get 4% interest).

Happy New Year to you and family.

Hi Rasid,

Especially in a low interest rate environment, if we can afford to do so, rather than using our CPF money, it makes sense to use cash to pay for our homes. :)

Once we turn 55, we can withdraw our OA and SA money in excess of the FRS but we have to withdraw all the money in the SA first before we are allowed to withdraw even the interest generated by our OA.

This is still a little known fact.

My plan is to continue to do Top Up and VC at least till I turn 55.

I might want to enjoy life a bit more after that or I could continue to stash away more money in the CPF. ;p

Thank you for sharing your experience. Happy New Year! :)

References:

1. Use CPF savings for homes and investments?

2. Withdrawing CPF savings: How much and how?

3. How much passive income is enough?

Thank you AK. On the following comment:

“Once we turn 55, we can withdraw our OA and SA money in excess of the FRS but we have to withdraw all the money in the SA first before we are allowed to withdraw even the interest generated by our OA.

This is still a little known fact”

Perhaps better to transfer my OA to my dad’s RA? I’m still deciding, maybe one of these days I drop by CPFB to seek their advice in person.

I also plan to do property pledge and just retain BRS in my RA once I reach 55. I can do the SA shielding in a DIY manner (ie not hvg to engage those financial agents to do it for me). But I think property pledge is less of hassle. The difference in interest loss is superficial.

Hi Rasid,

Helping our parents with retirement funding is always a good option. :)

As for 'shielding' of CPF, I have always said it is a loophole and CPFB might take action to plug it.

Anyway, like you said, the difference in interest loss is superficial.

Yes, best to check with CPFB on the options available. :)

References:

1. No more "shielding" of CPF soon?

2. How younger CPF members get 6% a year?

Hi AK

I will be moving 60K from my OA to my dad's RA.

Understand from CPFB that this amount will get average 5.5% interest

(6% on first 30K and 5% on next 30K).

Interest rate in RA is better than the 2.5% interest in OA.

I think this is something Singaporeans should consider doing, if they are able to, esp in this low interest rate environment (altho there's any upward pressure on interest rates now).

Hi Rasid,

That is a good plan especially if your dad's RA is sitting at zero or near zero balance.

Happy for you and your dad. :D

Reference:

Unfair FRS CPF LIFE payouts compared to BRS?

Angry with our Oracle AK71?

That has to be the gravest mistake anyone can make in his/her life.

It's as bad as cutting off his/her own 财路 !!

Akin to cutting off one's nose to spite one's face !

Hi Laurence,

I have had more than my fair share of encounters like that.

However, that particular encounter was very nasty and I just had to blog about it.

I do not claim to have all the answers.

There are many legal and moral ways to build wealth and we have to find our own way. :)

Hi AK

I have made $15K cash top up to my dad's RA. Saw that monthly payout will be $297 for four years. Wondering how CPF arrive at this figure. By the way, $297x12mthsx4years= $14,256 only. This is lower than the $15K top up that I made. And what about the interest earned? I wonder if anyone else facing the same situation can enlighten me, before I check with CPF.

Hi Rasid,

It does sound strange.

You might want to do an estimate before giving CPFB a call:

CPF calculators.

Reference:

CPF LIFE payout estimator.

Hi AK probably a better idea to top up CPF later in the month (e.g. 28th Jan) since CPF also states that the CPF interest rate based on the lowest balance of the month, instead of the average balance of the month.

There would be an opportunity cost incurred since that pot of money can earn interest sitting in a bank acct (e.g. from 1st Jan - 27th Jan)

Hi YJ,

Yes, I am aware of that but with interest rates so low, it really doesn't matter much. :)

AK! Happy New Year!!

May the Year of the Tiger roars in good wealth and health to you and family!

Hi rasid,

Wishing you a roaring good year!

Huat ah! :D

Post a Comment