In response to the lower than expected 4% p.a. yield in the 6 months T-bill auction which happened in the first half of this month in November, I expressed my disappointment.

I also expressed my disgust but maybe that was a bit too much as desperate people are just behaving like desperate people.

See:

4% yield T-bill 3.2x oversubscribed.

In that blog, I also wondered if the subsequent T-bill auction would see a lower yield with massive oversubscription expected once again?

It would be massively disappointing if the yield should be even lower than the promotional fixed deposit interest rates offered by the banks for a 6 or 12 months tenor.

If I am not mistaken, UOB offered 3.85% p.a. for a 6 months tenor fixed deposit while DBS offered 3.8% p.a. for a 5 months tenor fixed deposit recently.

Anyway, I decided to go ahead and give it a go.

Crossing fingers that we won't get too many low ballers dragging down the yield.

To be honest, I would be quite happy if the cut-off yield is 4% p.a. again.

Setting the bar pretty low given where promotional interest rates on fixed deposits are at.

Not setting high expectations means a lower chance of being disappointed.

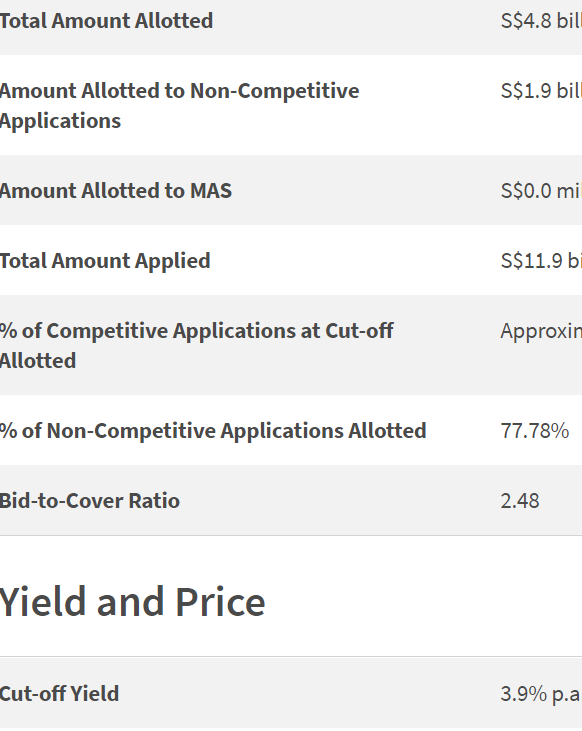

So, what's the result?

Cut-off yield for the latest 6 months T-bill auction:

Only 3.9%!

This is only slightly better than the best fixed deposit promotional interest rates we have seen lately.

As if Mr. Market was expecting the yield to be rather uninteresting this time, this T-bill auction was "only" 2.48x oversubscribed!

Now, do I apply for more T-bills in December or just stick with fixed deposits? I am leaning towards fixed deposits if the banks' promotional interest rates remain relatively high. Greater transparency. Zero suspense. Better for my weak heart. However, if fixed deposit promotional interest rates become less interesting too, then, I could try to get some T-bills again next month. Related post:

Source: MAS

Growing passive income.

Bloggy Award

Bloggy Award

9 comments:

I applied this round too, with a bid of 4.1%. Well, not that disappointed that I didn't get though, LOL 😆

Hi Sandra,

I agree.

You didn't lose anything. :D

CIMB now offers 3.9% p.a. for 12 months FD and 4.2% p.a. for 18 months FD.

4.2% is better than the CPF Special Account's 4%.

So, I decided to park some money there.

18 months is pretty short compared to what the CPF Special Account requires. ;p

Very true 😊

Hi AK71

For these using CPF if the bid too low and the success result is lower than 2.91 percent then it will be lower than CPF interest for 7 months as one has to factor for the withdrawal and return of fund from CPF.

Likewise if auction fall in between 2 months the breakeven is 3.33 percent.

Don't understand why someone will bid very low.

Unless my logic is wrong

Hi AK, do u invest in Frasers L&C Tr ? Any thoughts to it? Value to buy?

Hi Aa,

I agree with you.

For those who are using their CPF-OA money to bid for T-bills, they might fear not getting full allotment because it would mean more cost in terms of time and CPF interest income lost.

In fact, taking part in a T-bill auction which happens in the second half of a month with CPF money could mean losing 8 months of CPF interest income and not 7 months as there is probably going to be some time lag when the T-bill matures and the refund of money into CPF IA and then into CPF OA.

However, a strategy of putting in very low bids not only does harm to others, the low ballers also run the risk of getting a cut off yield which might not make sense or, if it makes sense, the difference in interest income might not be significant.

Desperate people do the most asinine things.

Hi S A,

I blogged about it a few months ago.

It is one of my better investments:

Frasers Logistics Trust: Another largest investment.

At the time, I warned that I would add only if its unit price fell by another 10% or more.

I meant I would wait for it to go under $1.20 a unit.

Turns out I was right.

To buy or not to buy?

Don't ask me.

I blur lah. ;p

Hi AK, thanks for your comments.

Would u blog about Parkwaylife reit? Given the share prices haven been depressed from its high. What r your opinions to it?

Hi S A,

Nope.

I have zero interest in Parkway Life REIT.

A distribution yield of 3.5% when the risk free rate is rising rapidly just doesn't cut it for me.

Still trading at a huge premium to NAV too.

In the current environment, I feel that there is more downside risk than upside.

I have always felt that people were paying too much for it and although the unit price has come down, to me, the REIT is still expensive.

Don't understand the fascination people have for the REIT.

I would rather invest in DBS, OCBC and UOB. ;p

Post a Comment