For readers who who are not subscribed to my YouTube channel or who simply prefer reading blogs to watching videos, this is the transcript of the video I produced yesterday.

------------

Not too long ago, I said that a cut-off yield of 3.78% per annum for 6 months T-bill was decent enough.

I was quite happy that the cut-off yield was still much higher than what DBS, OCBC and UOB offered for 6 months fixed deposit at the time.

I still feel the same way now.

Of course, if we are using CPF funds to buy T-bills, the sensible thing to do would be to benchmark the cut-off yield against interest rate offered by OCBC for fixed deposits placed using CPF OA money.

With a promotional rate of 3.3% per annum offered by OCBC for such fixed deposit placements, it boggled my mind that there were people placing competitive bids lower than that.

With T-bills yielding much more in the USA, it is strange that T-bills in Singapore should have much lower yields.

This suggests to me that Mr. Market feels that the Singapore Dollar is stronger and safer than the US Dollar.

It is just an impression as I don't know enough to tell if this is true, especially when it seems counter intuitive.

Anyway, with the debt ceiling issue in the USA, T-bill yields have been going higher recently.

In Singapore, I also noticed this.

In case you are wondering, I visit Monetary Authority of Singapore's website to look at the Treasury Bill Original Maturity table regularly.

This gives me a feel of where T-bill yields are going in Singapore.

A higher proportion of fixed income will help to reduce portfolio risk and volatility.

Constructing a T-bill ladder to create another source of passive income is also viable with interest rates being much higher.

We will see T-bills maturing every 2 weeks or so and receive some income when we recycle the returned capital into new T-bills.

If you are interested to look at the Treasury Bill Original Maturity table, see link to the website and table I have provided below.

If you are interested to look at the Treasury Bill Original Maturity table, see link to the website and table I have provided below.

Of course, I remind myself that the yields we see in the table are only suggestive because it assumes that participants will be rational in upcoming auctions.

With more retail participation, and with quite a few bloggers recommending their readers to place competitive bids way below average in order to secure their T-bills, the cut-off yields for future T-bill auctions could still surprise on the downside.

This is especially for T-bill auctions happening in the first half of any calendar month.

This is because we are likely to see lower participation from retail investors using their CPF OA money for auctions taking place towards the end of any month.

They run the risk of losing 2 months' worth of CPF OA interest instead of 1 month for auctions happening towards the end of a month.

I might complain about low balls, but I have to accept this uniquely Singaporean reality if I want T-bills to be a part of my portfolio.

Anyway, I am mostly recycling money from maturing T-bills into new T-bills as my T-bill ladder is complete.

The front end of the yield curve is likely to stay elevated for some time.

So, I continue to expect 6 months T-bills to remain relatively rewarding in the near future, especially when taking into consideration that it is risk free and volatility free just like the CPF.

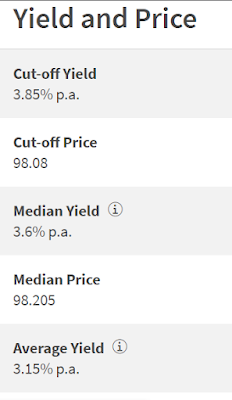

I am quite pleased with today's T-bill auction's cut-off yield of 3.85% per annum.

I am quite pleased with today's T-bill auction's cut-off yield of 3.85% per annum.

I know that some people look down on T-bills or anything that provides a return that is lower than the inflation rate.

If these people are very rich and have a lot of spare cash sloshing around, they can look down on T-bills, if they like.

The very rich can afford many things and snobbery is one of these.

However, for most of us, accumulating a meaningful amount of cash and cash equivalents is more a need than a want.

Warren Buffett said unless we are very rich, don't go around spouting nonsense like "cash is trash".

People who look down on T-bills and the returns should remember that T-bills are volatility free and offer risk free returns.

We should not compare them with potential returns from investing in stocks, for example.

I still say that before we start investing, we should learn to be better savers.

I am glad to save for passive income even as I invest for passive income.

If AK can do it, so can you!

Reference:

Treasury Bill Original Maturity.

Treasury Bill Original Maturity.

Bloggy Award

Bloggy Award

4 comments:

Dear AK

Interesting indeed

The reason for the yield disparity of local T-bills as compared to US T-bills is due to two reasons

A- There is something called the “pass-through” rate correlation. This has historically been close to around 70%

This means that when the fed raises or drops, we do not get a one to one move but closer to 70% of the move

B- Currency moves as well, to a lesser extent, influence this. Primarily as the USD is a safe haven for global funds. Any perceived insecurity or instability and the USD is favored, further increasing the gap

C- Whenever there is demand for fixed income, short term yields go much higher due to sheer demand for US treasury bills which is obviously not the case elsewhere wherein fixed income markets have limited depth

As regards T-bills, they should NEVER be compared with equity as RISK FREEDOM is the basic tenet of investments here

Finally, it all boils down to investor risk appetite and temperament, and most do not want a sub inflation return. This is understandable but their option then would be to control itchy fingers and stay in hard cash or money market funds wherein they have instant access to pounce on market opportunities

Lastly, active employment with high disposable incomes often fosters this attitude and I must say, if they are prudent equity investors, they can afford to lose money but make more overall than in fixed income instruments over time. This is the main issue. Ultimately, behavioral traits influence investing decisions as well!

Regards

Garudadri

Hi Garudadri,

Thanks for the explanation. :D

I understand point A as we import interest rates from the USA but not get a 1 to 1 translation.

As for points B and C, the debt ceiling debacle might have undermined confidence in the US$ and also reduced demand for US T-bills which led to higher yields.

However, although this is understandable due to event driven confidence issues, it is curious to me that US T-bills would yield a full percentage point more than SG T-bills even during uneventful times.

I smiled when you said "itchy fingers" as I know the feeling.

There were times in the past when I was sitting on a lot of cash and my fingers got itchy. (TmT)

For sure, lacking an earned income, much less a high disposable income, retirees like me should be more conservative in money matters.

This chat is a nice change from our usual chats on investing in banks and REITs. :)

Helps my brain to wake up in the morning too. :D

enjoy and love these T-bills' high yield while we can. no brainer.

Hi cbd,

I also say. ;p

Make hay while the sun shines. Huat ah! :D

Post a Comment