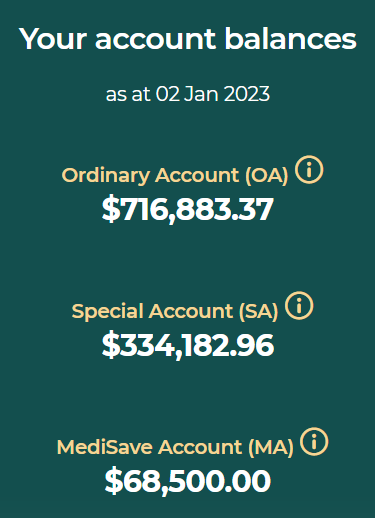

Last year, it was almost $1.1 million in CPF savings.

This year, it is more than $1.1 million in CPF savings.

Confession.

AK cheated last year.

That almost $1.1 million included voluntary contributions to my CPF account made at the start of 2022.

Terrible AK!

This year, AK is turning over a new leaf.

No cheating.

More than $1.1 million in CPF savings at the start of 2023 all thanks to full year interest earned in 2022.

What is more satisfying than making money?

When the government is making money for me lah.

Kamsiah plenty plenty to Ah Kong.

Ah Kong will be doing some heavy lifting again for me this year.

To be exact, Ah Kong will be doing all the heavy lifting for me this year.

Why like that?

AK lazy again?

Ahem.

I won't be making voluntary contributions to my CPF account this year as all the money has been used to get Singapore Savings Bond in 4Q 2022.

So, my CPF account will not be growing as much as I won't be helping to grow it.

Might not be making voluntary contributions next year in 2024 either as I could use the money to get Singapore Savings Bond again.

See:

CPF or Singapore Savings Bond?

My YouTube video:

The condition is, of course, that Singapore Savings Bond continues to offer more than 3% per annum in 10 year average yield.

So, I am going to pass on the latest Singapore Savings Bond as it is only giving 2.97% per annum in 10 year average yield.

|

| Source: MAS |

What if the 10 year average yield stays lower than 3% per annum for the whole of 2023?

In such an instance, I would go back to doing voluntary contribution to my CPF account.

I could do this in December 2023 instead of waiting till January 2024 since I would not have made any voluntary contribution in 2023.

However, I am still topping up my CPF MA in 2023 as it pays 4% interest per annum.

My YouTube video:

In fact, I just did it.

Before topping up CPF MA:

After topping up CPF MA:

Could top up only $2,500 to the CPF MA as the latest Basic Healthcare Sum (BHS) is $68,500 only.

I know some people say that the CPF is a national PONZI scheme.

Do PONZI schemes ever set a cap to how much money their clients can pump in?

I blur.

How like that?

See:

The CPF is really a national PONZI scheme!

Some people say that their CPF account is losing money.

I blur.

Let me rub my eyes and look again.

Quite sure my CPF account did not lose any money.

In fact, my CPF account made more than $33,000 for the whole of 2022 while I did literally nothing.

Alamak.

You still rubbing your eyes and looking?

OK, enough looking.

Move along.

Nothing to see here.

Early Chinese New Year ang bao from Ah Kong!

Gong Xi Fa Cai!

Huat ah!

References:

1. Almost $1.1 million in CPF savings.

2. 2022 passive income: Resilience.

3. SSB: Mission accomplished.

Bloggy Award

Bloggy Award

13 comments:

Hi AK,

Congrats on your > 1M4X achievement. I am still trying to max out my SA and hope to achieve that a couple of years time. 1X more years before I hit 55, not enough time already. I will also be starting to top up my kid's MA in a monthly basis.

Looks like China opening up is going to boost HK market a lot, can see that in recent market prices. Any plans to add a bit more HK index ETF?

Hope you have a HUAT 2023!

Hi AK

I like your XXL-size pie. My own pie isn't too shabby, should be able to grow to XXL-size like yours, if I remain gainfully employed for the next decade. I have also topped up the MA, so that any other mandatory contributions woud continue to help grow my OA.

Agree with you that the SSB this time round is not at all attractive. Nibbling in bank shares and FDs instead.

Hi keng,

Although I encourage all CPF members (below the age of 55) to hit the prevailing Full Retirement Sum in their Special Account, all of us have different circumstances.

I like your idea of topping up your child's MA. :D

As for the Hang Seng Tech ETF, as you probably know, I am so lazy to trade stocks these days.

I still have a position which I am holding on to.

In the short term, the immediate support is probably 71c which was resistance before.

The stronger support is at around 65c which is where the 50 days and 100 days moving averages might form a golden cross.

If it goes to 65c, I might add some. ;p

Wishing you a HUAT 2023 too! :D

Hi Yv,

I like pies and the CPF pie looks yummy. :D

Yes, please stay gainfully employed and don't be lazy like AK.

If everyone is economically inactive like AK, the economy will be very cham. -.-"

One of the things I miss about being gainfully employed is CPF mandatory contribution, to be honest.

Can't have my cake and eat it too, I know. ;p

Investing for income the way you do can hardly go wrong.

Gambatte! :D

Hi AK,

I appreciate your sharing, especially on CPF matters as I know nuts about growing my money via the stock market. You kept me motivated to work towards hitting my FRS in SA and now hopefully at 55 I will not be too far away from ERS if I can hold on to an average-paying job. I am nowhere near financial freedom but hitting FRS is a big relief.

Once again thank you and may 2023 bring you health and happiness.

Hi Unknown,

For most of us, the CPF is not only a cornerstone of our retirement funding but the foundation of our retirement funding.

I remember saying that the CPF is a low hanging fruit that all CPF members should take full advantage of. :)

Thanks for sharing the progress you have made in hitting the FRS in your CPF SA.

Next step, ERS!

Wishing you good health and abundant joy in 2023. :D

References:

1. How to turn $60K into $332K?

2. Choose your own CPF adventure.

Sheena Choy said:

Your OA is huge. You top up using VC3A? You can move OA to SA for higher interest?

AK said:

I did VC3A faithfully for many years but I won't be doing it this year.

Cannot do OA to SA transfer anymore. Have not been able to do it for many years as my SA exceeds the prevailing Full Retirement Sum.

I did OA to SA transfer in the first few years of my life as a working adult to give compounding more time to work its magic:

Upsize $100K to $225K.

Sheena Choy said:

oh ya it hit FRS. Did you use OA to buy house?

AK said:

Many years ago, I did. I sold and refunded all the money used to my OA.

See:

How did AK amass so much money in CPF OA?

Hi AK, question about CPF interest, as I'm working on some projections for my own cpf.

I am aware that the CPF interest for MA flows to SA account if u exceed the prevailing BHS

but does SA interest flow out into OA account if u have exceeded the prevailing FRS (i.e. FRS of people turning 55 in the same year)?

Hi zhenling,

Interest earned in MA flows into SA but if the SA has hit FRS, then the interest earned in MA goes into OA.

Interest earned in SA stays in the SA even if the SA has hit FRS.

So, a retiree who has no mandatory contributions but leaves his CPF SA untouched will still see his SA balance growing annually.

Very fortunate for AK. ;p

thanks AK!

based on the published BRS for cohorts turning 55 from 2017 to 2027, I estimate that BRS has been increasing about 3% every year.

without any new information from CPF, I assume(*!!) the BRS 3% increment to be constant further into the future. that makes the 4% interest from SA and RA accounts very attractive. I estimate that hitting prevailing FRS at age of 45 would almost guarantee hitting projected ERS by the time one ages to 65. That's a pretty manageable goal, for someone gainfully employed until 45.

*-I have to make some assumptions since the BRS has not be published for my cohort.

Hi zhenling,

I agree that a 3% increase per year is a good estimate.

I also agree that hitting the FRS by age 45 is fairly doable as long as that someone is not paid too little and is financially prudent.

Let the government help us to hit the FRS in our CPF SA. ;)

If AK can do it, so can you! :D

References:

1. Retiring by age 40 is a fantasy?

2. A lot of money in my CPF SA is from the government.

Hi AK,

are you still holding on to any hang seng tech etf and is now still a good time to enter to earn some extra cash?

Hi SL,

If you read my past blogs on Lion OCBC HS Tech ETF, you would know that this is for trading.

That is the only way to make money from this since it doesn't pay any dividend.

So, if you are interested, you really must know some technical analysis and be looking at the charts quite a bit to make trading decisions.

We cannot ask if this is good value for money now, buy and forget while collecting dividends.

For me, I have made money on three trades already and still hold a small position at a low cost.

I am just speculating with this small position that the unit price could go quite a bit higher in future.

The unit price now seems to be going sideways and seems to be drifting slightly lower but the momentum oscillators have turned up.

So, we could see unit price rising but it has multiple resistance levels to clear along the way and if it could break 69c, it could go much higher.

If I am planning to buy more, 58c to 62c seems to be a good zone to enter.

Post a Comment