Whenever I blog about the CPF, I must be prepared for some debate and it happened again last night.

I always welcome debates as long as they are civil and constructive.

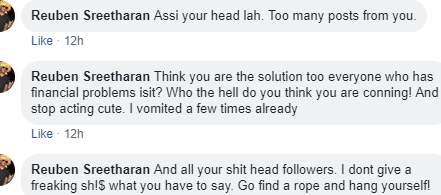

Please don't be rude.

Don't tell people to get a rope and hang themselves, for example.

I am so sorry to have caused the reader so much angst. :(

Since following my blog upsets him, I will do him a big favor by blocking him.

I don't usually block or ban readers from my FB page.

If I did it to you, you must have been pretty bad.

Don't follow my blog.

Don't worry. Be happy. :D

I am glad to share an example of a civil debate with another reader here.

Reader says...

Our CPF removes choice.

One may suddenly need money for some valid reason eg temporary retrenchment but one will not be allowed to take out even a small sum to meet daily needs.

Malaysia's EPF and Singapore's CPF have some good aspects.

EPF is like a bank which allows withdrawal of money when needed but the same bank tells CPF subscriber that no money can be released whatever the need however urgent.

Would you put your hard earned cash in such a bank for it to dole out paltry sums now and then saying its looking after your money for old age?

While CPF is good , it needs a little flexibility in disbursement of funds which after all belong to the subscriber.

What use are better returns when one cannot enjoy them at will and perhaps will only be given to your nominee on your demise?

AK says...

In reply to: "Would you put your hard earned cash in such a bank for it to dole out paltry sums now and then saying its looking after your money for old age?"

Such a comparison is misleading.

I think we have to be clear what the CPF is.

CPF isn't a bank although we can use it like one when we turn 55 if we have the FRS in the CPF-RA then.

For people who do not even have the FRS (or BRS) in their CPF accounts and wish to draw upon their CPF savings whenever they have a financial bottleneck, they need to do serious financial planning pronto.

Also, CPF LIFE is not a bank that doles out a paltry sum.

The comparison is again misleading.

Once your savings in a bank runs out, you are out but not with the CPF LIFE which pays you for life.

In reply to: "What use are better returns when one cannot enjoy them at will and perhaps will only be given to your nominee on your demise?"

It is precisely this type of thinking that leads to "Return Our CPF" rallies in Hong Lim Park.

Many people who supported the rallies had very little savings and yet they wanted to utilise their CPF (retirement) savings "to send children to study overseas", "to go on a holiday", "to go on a pilgrimage" etc.

The higher interest rates in our CPF-RA is to help us better fund our retirement and not to be depleted at a whim which is what many would do if given a choice.

See the latest comments in the following blogs:

1. Retirement funding assurance for average investors.

2. When to get a private annuity.

3. Food inflation in Singapore and Malaysia.

4. We do better at managing our savings than CPF does.

Related posts:

1. Crazy Rich Asians or Pragmatic Rich Asians?

2. Use CPF as a savings account.

Bloggy Award

Bloggy Award

{kind=link}