The week started with the shutting down of Silicon Valley Bank and Signature Bank by U.S. regulators.

The U.S. regulators announced measures which ultimately bailed out the banks.

Then, we saw Credit Suisse reporting "material weaknesses" and the Swiss National Bank stepping in to backstop the troubled bank.

Credit Suisse took a 50 billion Swiss Francs loan from the Swiss National Bank to strengthen liquidity.

Then, a consortium of 11 largest U.S. banks rescued First Republic Bank, the 13th largest bank in the U.S.A., by jointly depositing US$30 billion in the troubled bank.

After all that happened, Mr. Market ended the week with a dramatic down day in the U.S. stock market on Friday.

The Fed increased interest rate a year ago in March 2022 for the first time since 2018.

Since then, the rapid rate at which interest rates have been increased has caused a lot of pain for homeowners as well as investors in the real estate space.

The pain is most keenly felt in the high growth but negative earnings tech space and if you are a tech investor, you know this firsthand.

The people who said that something would break under the growing pressure of such rapid rate hikes are now looking rather prescient.

What would they say now?

Not surprisingly, that things will continue breaking as long as the Fed continues to hike interest rates.

With the ECB having hiked interest rates in the EU by another half a percentage point, the Fed is probably going to hike interest rates in the U.S. next week too as they stick to their plan to fight sticky inflation.

Mr. Market, already jittery, while initially assured by the show of solidarity in the U.S. banking industry, became depressed again on Friday when First Republic Bank suspended dividends.

In an environment where depositors could lose their savings and where investors in both stocks and bonds are losing money, heightened volatility in the stock market is unsurprising.

Fear is palpable.

It drives Mr. Market into self-preservation mode.

If the confidence deficit continues, then, more money could flow to the perceived safety of U.S. government bonds, and we could see yields lower.

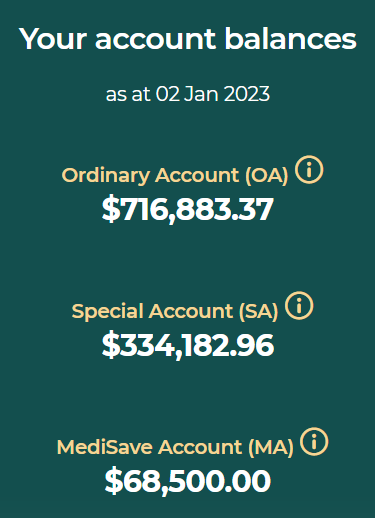

During the COVID-19 pandemic, I blogged about how I was worried because my passive income was reduced due to my businesses either suspending or reducing dividends.

My relatively high level of CPF savings was the only "investment" that continued to pay what I expected it to pay, uninterrupted, which highlighted to me the importance of having an allocation to high quality fixed income in any portfolio.

So, I can understand Mr. Market's negative reaction to First Republic Banks's decision.

Many people depend on dividends for a living or to at least fund part of their expenses.

The still troubled bank saw its stock price recovering from a day ago on Thursday only to see it plunging 32% on Friday.

When the bear comes out of its cave, none is spared, and we saw the stock prices of large U.S. banks beaten down too as even JP Morgan saw a 3.78% decline in its stock price.

When Mr. Market is gripped by fear, he becomes irrational, and the baby gets thrown out with the bathwater.

As U.S.A. is still the largest economy in the world, what happens there often spreads to the global markets.

So, we could see Asian markets echoing that fear in the U.S. stock market.

I have said many times before that we cannot predict what will happen but if we are prepared, we need not worry and we could instead benefit.

Don't be overly pessimistic.

Don't be overly optimistic.

Be pragmatic.

This week, I was on steroids.

I have published too many blogs regarding the stock market and what my plan might be.

So, if this is your first visit in as long a time, you will have a lot to read.

Have a good weekend.

Recently published:

US$30b rescue! T-bills 3.65%! Banks or REITs?

Ticketing for "Evening with AK and friends 2023" is ongoing.

US$30b rescue! T-bills 3.65%! Banks or REITs?

Bloggy Award

Bloggy Award