Ever since the CPFB introduced a colorful pie chart of our CPF savings a few years ago, I would look forward to mine every year like a teena...

Past blog posts now load week by week. The old style created a problem for some as the system would load 50 blog posts each time. Hope the new style is better. Search archives in box below.

Well, I am trying different things in Genshin Impact such as putting different characters in a team to see how things work out for them.

Oh, you mean doing things differently in the stock market?

Oops.

I haven't done anything.

So, what's there to say about doing things differently?

Nothing.

If we are investing in good income producing assets, there is really nothing much to worry about.

I can continue gaming and not look at the stock market for many years in a row and these assets will probably still be generating income.

There is, however, a big "IF."

If we did not invest with money we cannot afford to lose which includes debt in all its forms...

Mr. Market will have mood swings and there is really no telling why and when these mood swings happen.

When Mr, Market's mood swings happen, stock prices usually see big moves.

Plunging prices shouldn't matter to us if we are invested in good income producing assets as long as we are not investing with money we cannot afford to lose.

Then, there are speculators.

Speculate only with money we can afford to lose.

If we cannot afford to lose a single cent or don't like the idea that we could lose money, don't speculate.

Remember, Mr. Market can stay irrational far longer than we can stay solvent.

Remember, don't risk losing the things we need for something we really don't need.

Remember, nobody cares more about our money than we do.

We don't want to have to liquidate at prices we would usually have rejected.

We don't want to be at the mercy of Mr. Market.

After all, Mr. Market is not known to be merciful.

When the tide goes out...

So, why am I able to keep cool and continue gaming?

It has been more than a month since the last time I blogged.

I have been spending most of my time in Genshin Impact in the last month but I also took several days off from gaming to attend to stuff in real life.

I will be taking a few days off from gaming to spend more quality time with my parents again this month too.

In my retirement, I try to keep things as simple as possible.

Keeping things simple is seen in my investment philosophy as well as I mostly invest for income and avoid active trading which requires more time and energy.

Investing in good income generating entities which have the ability and willingness to reward their investors is a good way of avoiding emotional roller coasters too.

If you believe that peace of mind is priceless like I do, then, investing for income is probably right for you.

GONG XI FA CAI

So, is investing for income easy?

Is it just about looking for investments which offer the highest yield?

Ahem, have you read about Eagle Hospitality Trust (EHT?)

If you haven't, I have a series of blogs on EHT and one of them is about a reader's experience.

Of course, we cannot be right all the time as even the best of plans can go wrong.

However, if we know what to look out for, we can definitely make better decisions.

If you have been following my blog for a long time, you will know that I share my philosophy and methods openly.

You would probably have an idea of how I go about investing for income.

However, it is all rather piecemeal.

I have been told by quite a few people that my blog is disorganized but if someone is willing to do the legwork, learning how to invest for income just by reading my blog might almost be doable.

For people who do not have the inclination nor the time to comb through my blog, then, attending an inexpensive and well designed course on investing for income is probably a better idea.

Dividend Machines is the only course on investing for income I have ever promoted.

I even attended the course myself when it first launched so many years ago.

Investing for income is an important reason why I am able to have more time to do the things I enjoy.

Investing for income is an important reason why I no longer even have to work for a living.

Financial freedom isn't impossible.

Early retirement isn't impossible.

What I have achieved might seem magical to some but investing for income really isn't magic.

Run by good people, Dividend Machines is not only well designed, it is also inexpensive and provides great value for money.

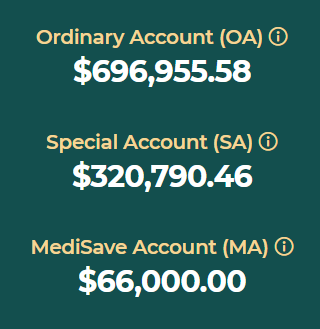

Since the reader's focus seems to be on CPF funds withdrawal at age 55, it should be interesting to note that any excess interest income generated by our MA will flow into our Special Account (SA) or into our Ordinary Account (OA) if our SA has hit the Full Retirement Sum (FRS.)

For me, it flows into my OA.

See:

Since the MA has the same interest rate of 4% as the SA, this mechanism makes it attractive as an additional income generator since money in the OA and SA can be withdrawn once we have set aside the FRS in our Retirement Account (RA) at age 55.

Some readers might also be interested in this blog:

How time flies and it has been more than 5 years since I became a retiree, just a few months before I turned 45.

In my case, financially, the biggest negative aspect of being a retiree is probably the lack of mandatory CPF contributions.

I mean my passive income is large enough to replace my past earned income and then some.

So, I suppose my cash flow is healthy enough.

However, as I believe in growing my CPF savings so that it continues to act as a meaningful bond component of my investment portfolio, I would do Voluntary Contribution every year to the maximum allowed.

Yes, I have been growing my CPF savings without any help from mandatory CPF contributions which those who are employed receive.

Makes me wonder if I should return to the workforce?

Exchange my time for money again?

Lazy me working again?

PTSD!

Of course, even in my retirement, I was not able to do any Top Up to my CPF account as my CPF SA has exceeded the prevailing FRS.

Year after year, the interest earned by money in my SA would exceed any increase in the prevailing FRS.

Yes, without me having to do anything, my SA stays above the prevailing FRS.

In my case, I am interested in pumping as much cash as possible into my CPF account.

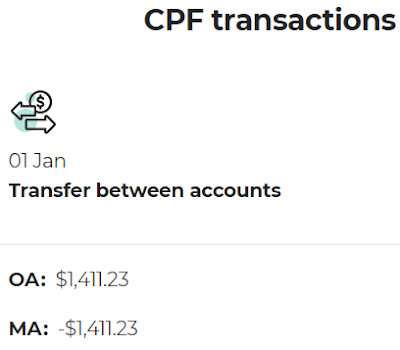

So, for maximum cash injection into my CPF account, I first did a $3,000 Top Up to my MA to hit the new BHS of $66,000.

Then, I did a Voluntary Contribution or VC3 (i.e. VC to 3 accounts) that is equivalent to the CPF Annual Contribution Limit of $37,740.

The order is important because if I had done the Voluntary Contribution first, then, the money would have flowed into my OA, SA and MA, leaving less room to Top Up my MA.

As I did the Top Up to my MA first, I could inject more funds in total to my CPF account and money from the Voluntary Contribution or VC3 flowed only into my OA and SA, effectively becoming VC2.

AK so witty.

Compared to the last few years, total voluntary cash injection into my CPF account this year is higher at:

S$ 40,740.

Those of you who complain that AK has not been giving 4D might see a potential 4074 here.

Kidding!

I have said it countless times but CPF members are a fortunate bunch.

Albert Einstein said compound interest was the 8th wonder of the world.

However, as many people do not have passive income that is sufficient for them to stop working, it is a good idea for them to have disability insurance.

For this group of people, Careshield Life is a better product than Eldershield for the following reasons:

1. Lifetime coverage.

We only need to pay till we are 67 years old or for 10 years after joining, whichever is later, and we are covered for life.

2. Lifetime cash payouts.

We get monthly payouts for as long as we are severely disabled while Eldershield only pays for up to 6 years.

3. Payouts increase over time.

Eldershield pays a fixed amount of $400 a month while Careshield Life pays $612 a month and it will increase at 2% per year.

Low income families probably need Careshield Life the most and they will receive significant subsidies.

For those of us who are older, we will get incentives for joining Careshield Life by 31 Dec 2023.

I received a letter from the Ministry of Health to automatically enroll in Careshield Life last month.

Based on my age, I will get a small incentive to do so too.

Since I was already enrolled in Eldershield to help lower the cost of collective risk sharing at the suggestion of a friend, I went with the automatic enrollment.

Careshield Life is a low cost disability insurance product.

For me, the premium is $200+ in the first year after subsidy and incentive.

I also like the idea that I am doing some good for society with my enrollment.

For anyone who is interested in finding out more, do a login with your Singpass at:

To be fair, although self insurance is probably the best form of insurance, we can never tell if our passive income could be impacted negatively at any point in time.

So, having some disability insurance is probably not a bad thing even for those of us who have the best insurance in life.

So, I am compensating by being a few days earlier with this one.

Also, several things which will need my attention in real life have popped up next month in January.

Unfortunately, they are likely to be very time consuming.

As I still want to spend much of my time in virtual worlds, I might not have much time left in January for blogging.

Neverwinter is launching a new module, Dragonbone Vale, on 11 January but until then, I will be busy in the worlds of Black Desert Online and Genshin Impact.

I am really enjoying Genshin Impact and can imagine losing myself in that world for some time to come.

I blogged about retiring in 3 virtual worlds a few months ago and that included Guild Wars 2.

Genshin Impact has replaced Guild Wars 2 for me.

The 3 virtual worlds for me are now Neverwinter, Black Desert Online and Genshin Impact.

I wish I have many more hours in a day but, sadly, I don't have enough hours each day for more than 3 virtual worlds unless I abandon the real world.

I did not plan on blogging again until the new year when I would share my 4Q 2021 results.

I would also probably have blogs about the CPF sometime in January.

However, the reader who wrote to me about his purchase of Alibaba shares at $220 a share after reading blogs by a local blogger left me another comment.

For those who are clueless as to what I am talking about, read:

Anyway, after reading the reader's latest comment, the blogging bug bit me and the result is this blog.

Alibaba's share price continues its slide and the downtrend is pretty much intact.

It should be obvious even to those who are not technically inclined that the downtrend is pretty persistent.

Many have been cut very badly by falling knives and some have had their fingers or hands cut off.

There are many who are still holding on in the hope of a reversal so that they could make a lot of money eventually.

However, they should bear in mind that there are many stale bulls who are waiting for a lift in prices so that they could sell to break even or to reduce their losses.

It is only reasonable to expect some strong resistance or those holding on could be setting themselves up for more disappointment.

So, investing in Alibaba Group now is to invest in a downtrend and to hope for a reversal that is likely to be full of obstacles.

It is definitely not for the faint hearted and those who do not have deep pockets.

This is especially the case when Alibaba does not pay dividends.

So, to say nothing of the capital loss, the opportunity cost for investing in Alibaba is pretty high.

Alibaba's investors are not being paid to wait for things to get better.

What to do?

If the ever widening paper loss is making us lose sleep, it is probably a good idea to reduce exposure.

Using money we cannot afford to lose or borrowing money to invest in such a situation is probably a sure way to get insomnia.

Those with anger management issues could even see familial and social ties affected.

What about those who have used money they can afford to lose?

Well, they are more fortunate because they only have to ask if they are willing to lose the money invested in the worst case scenario?

Now, to answer the reader's question in his latest comment, whether to cut loss now or to hold on, is there another question he should ask?

Yes, there is one more.

If he did not invest in Alibaba Group at $220 a share so many months ago, would he invest in Alibaba Group at $117 a share today?

Why should he cut loss now if the answer is "yes?"

Of course, in such a case, it would mean that the time to cut loss has come and gone for him.

If he wouldn't invest in Alibaba Group even at $117 today, it probably means that his opinion of the investment has shifted so much that a much lower price is needed to entice him.

In such a case, cutting loss and buying again when a reversal is in place might be a better idea than simply holding on and possibly losing his mind.

We should bear in mind that share prices flow down a river of hope in a downtrend.

Low could go lower.

The time to buy is probably when share prices move lower in an uptrend (i.e. buying the dips) or even when share prices test supports in a rangebound situation.

Investing in Alibaba Group now is to buy the downtrend but if you are a billionaire like Charlie Munger or if you are investing with only a small fraction of the money you can afford to lose, you probably don't have much to worry about.

Having said this, we can never make all the money in the world and there are more important things in life than money.

Peace of mind is priceless.

I will end this blog with a screenshot of my house in Black Desert Online which has been nicely decorated for Christmas.

When it comes to AA REIT's unit price, I can only say that Mr. Market will do what it wants to do.

I do not know why the unit price is where it is but I do know that AA REIT should continue to generate stable income for me.

If there is a dip in DPU, it is probably going to be temporary, everything else being equal.

In the grand scheme of things, over a longer period of time, inflation should see prices including asking rent going up.

As an investor for income, I do not usually invest in REITs for a few months only or even for just a couple of years unless I find out it was a mistake which has not been the case for AA REIT.

Why did I add to my investment in IREIT Global and not AA REIT?

You are right in your suggestion that it was due to IREIT Global's rights issues and the fact that my resources are limited.

Also, I want to add that price is not the same as value.

At $1.60 a unit, AA REIT was trading at a big premium to NAV but its unit price has retraced to a level that is closer to its NAV which means it is a better time to buy now than it was before.

However, IREIT Global is still trading at a pretty big discount to its NAV which helps to make it a more compelling buy.

Warren Buffett famously said that whether socks or stocks, he likes buying quality merchandise when it is marked down.

When we take into consideration that IREIT Global holds freehold assets while many of AA REIT's assets are in Singapore with relatively short land leases, the value that IREIT Global brings to the table now shines brighter.

Having said this, it is important to bear in mind that AA REIT and IREIT Global might both own buildings but they are in different sectors.

They are also in different parts of the world.

Not putting all our eggs in one basket is probably a good idea.

Of course, AK is just talking to himself here and, depending on our motivations, it might or might not be relevant to us.

The last time I had a blog on this topic was in April 2020.

Back then, Mr. Market suffered a dramatic breakdown and took quite a long time to recover.

After almost 2 years, it still looks like it will be a while more before we are out of the woods, no thanks to the new Omicron variant of COVID-19.

The world is the way it is because there are too many greedy people, too many selfish people, too many ignorant people and too many malicious people.

Very unfortunate but very often bad things happen because of irresponsible human behavior.

If we are not careful, we might see Singapore becoming a "true democracy" with people against vaccination marching in the streets which, of course, would give the virus opportunities to infect even more people and possibly mutate again.

I feel that having a choice is a good thing but social responsibility is more important because we live in a society.

If we are not part of any society, if we live all alone on an island, then, we are free from social responsibility.

Personal freedom of choice is plain rubbish if we choose to put everyone else at risk.

It is similar to what I said before in many blogs in the past about being financially responsible because we shouldn't be a burden to society.

Some readers might remember my blogs on those protestors in Hong Lim Park asking for their CPF money to be "returned" to them.

Anyway, before I digress further which I am inclined to do, here is the update.

Largest REIT investments (each $100,000 or larger in market value.)

My largest investment in a REIT used to be AIMS APAC REIT (formerly AIMS AMP Capital Industrial REIT.)

It has been overtaken by my investment in IREIT Global which used to be smaller in size.

IREIT Global is now my largest investment in a REIT as I added to my investment several times when Mr. Market went into a depression because of the COVID-19 pandemic and also due to rights issues to help the REIT fund acquisitions.

Just like AIMS APAC REIT, I believe IREIT Global to be well run.

Recently, for example, they were able to quickly fill up all 5 floors of a property which were being given up by an existing tenant.

I also like that the REIT's insiders have a big stake in the REIT.

So, it is unlikely that they would do anything to hurt unitholders' interest.

My second largest investment in a REIT and probably my oldest is AIMS APAC REIT.

Most institutional investors would gravitate towards bigger names with a pedigree such as Ascendas and Mapletree when it comes to industrial REITs.

However, I am a retiree and distribution yield is an important consideration as I am very much interested in cash flow but I try to be careful not to be blinded by high yields.

I have been invested in AIMS APAC REIT since the Global Financial Crisis and, looking back, it has been good to me as an investment for income.

Just like IREIT Global, insiders have a meaningful stake in AIMS APAC REIT and it is unlikely that Mr. George Wang would do anything to hurt unitholders' interest.

There is talk that ESR which has been gobbling up REITs in Singapore is planning to gobble up AIMS APAC REIT as well, having grown their stake in the REIT.

However, unlike ARA Logos, I doubt Mr. George Wang would consider a deal that is less than fair to AIMS APAC REIT if such a deal should ever be proposed.

My third largest investment in a REIT was Ascott REIT-BT and that was due to my earlier investment in Ascendas Hospitality Trust.

As I expected the COVID-19 pandemic to have a rather long lasting impact on the hospitality sector, I decided to sell down my stake significantly some time back.

For many months after that, I did not have a 3rd REIT which was greater than $100,000 in market value in my portfolio.

Of course, that changed when I significantly increased my investment in Sabana REIT after ESR's low ball offer to take over the REIT failed.

Sabana REIT is now my third largest investment in a REIT, making a comeback after many years of absence.

I do have investments in other REITs but my investments in IREIT Global, AIMS APAC REIT and Sabana REIT are my largest now, being the only ones which are above $100,000 in market value.

Together, I estimate that they generate a bit more than S$70,000 in passive income annually for me.

I have been saying for quite a while that I want a more resilient income generating portfolio and to be less reliant on REITs for income.

However, for income investors, REITs remain a relevant tool and this blog shows my continuing reliance on REITs for income.

Still, I like to think that I have a more resilient income generating portfolio now as I increased my investment in the local banks so that together they were at one time larger than my investments in IREIT Global and AIMS APAC REIT combined.

Since I increased my investment in IREIT Global due to its rights issues, my investment in the local banks together have become smaller than my investments in IREIT Global and AIMS APAC REIT combined but probably not by very much.

Anyway, I get the feeling that I could ramble on and, so, I should really end the blog.

Till the next blog, remember to stay vigilant and be socially responsible as we try not to give COVID-19 any room to grow.

My last blog on ComfortDelgro attracted some very thoughtful comments from readers and if you are interested, read them: HERE.

I said in reply to a comment that I have been trying to build a more resilient investment portfolio for a few years by now.

Most of this effort has been centered on increasing the size of my investment in the local banks.

I believe that I have strengthened my investment portfolio's resilience in the most recent bear market this way.

This short blog is in reply to the latest comment by a reader in the abovementioned blog.

The reader's comment was about Far East Hospitality Trust.

My reply:

Yes, just like SIA and even SIA Engineering, the hospitality sector has been hard hit by the COVID-19 pandemic.

With the latest Omicron variant, it doesn't look like things are going to improve by much anytime soon.

Buying into hope might be just as painful as buying into hype if things go very wrong.

I significantly reduced my investment in Ascott REIT-BT some time ago.

However, I still retain a smallish position and that exposure to the hospitality sector is enough for me.

Having a larger exposure to the hospitality sector might give outsized returns if the pandemic subsides soon, of course.

As the ongoing COVID-19 pandemic has shown, however, a larger exposure does not make for a more resilient portfolio especially if we are mostly investing for income.

This is especially the case when we are buying into REITs and business trusts which pay out almost all their operating cashflow to their investors.

This is unlike businesses which pay out a fraction of their earnings as dividends to their investors.

With interest rates more likely to rise than not in future, we might want to invest in businesses that will benefit from rising interest rates instead.

As always, it is never my way or the highway.

Have our own plan and we should keep it grounded with realistic expectations or at least try.

Of course, even the most well thought out plan could go wrong.

If we must gamble, make sure the bet will not sink us financially and degrade our lifestyle if things do not go our way.

AK is just talking to himself and seems to have gone off topic.

Anyway, remember that the COVID-19 virus is still here in all its mutations.

Continue to be cautious and stay safe to keep all of us safe.

Omicron Covid variant spreads 'more than twice as fast' as Delta - BBC News

To stay invested or not, we will have to ask if the problems they are facing now are temporary or are they here to stay?

I am inclined to believe that the problems will not be permanent.

However, now we have the Omicron variant of COVID-19 that recently popped up.

So, it could take longer before a sustained recovery happens.

In my analysis done a few years ago, I said that even if ComfortDelgro were to shut down its taxi business, it would still be able to pay an attractive dividend.

That was partly how I made the decision to invest in ComfortDelgro as an investor for income.

Shutting down a business if it is no longer viable is not a bad thing, generally speaking.

I like to think that we will eventually conquer the COVID-19 virus.

However, the slow rate of vaccination in many parts of the world as well as irresponsible behavior such as vaccine hesitancy is allowing the virus to mutate.

These are some root causes for uneven recovery and a delay in sustained recovery.

Still, I am staying invested in ComfortDelgro and getting paid while I wait for the eventual recovery.

Bloggy Award

Bloggy Award