Ever since the CPFB introduced a colorful pie chart of our CPF savings a few years ago, I would look forward to mine every year like a teena...

Past blog posts now load week by week. The old style created a problem for some as the system would load 50 blog posts each time. Hope the new style is better. Search archives in box below.

That was about 6 years ago but I think some bits are still worth reading.

My gut feeling is that mortgage rates will rise faster than the SSB's 10 year average coupon.

Even the fixed deposit rates are rising rather quickly now as banks have started competing for deposits.

Banks are trying to lock savers in with higher rates now because they think interest rates will go even higher in future.

My mom went to renew her fixed deposit a few weeks ago and was pleasantly surprised to be offered 1.1% for 1 year.

This was because my aunt did her renewal a month before and she was offered 0.8% at the same bank.

Another bank offered my mom 1.5% per annum but it was a 2 years fixed deposit.

For a 3 years fixed deposit, they offered her 1.9%.

That's too long and we are not compensated enough when interest rates are expected to rise rapidly in the next couple of years.

I told my mom to just go with the 1 year fixed deposit because interest rate would probably continue rising rapidly.

We could soon see 2% interest rate offered for a 1 year fixed deposit.

In fact, it could even go higher if inflation stays stubbornly high and the Fed has no choice but to continue raising interest rate to a point where it is higher than the inflation rate.

After all, the most effective way of bringing down inflation if past experience is anything to go by is to have interest rate higher than what inflation is and inflation is at about 8% in the USA now.

We can say that inflation is lower in Singapore but, unfortunately, when it comes to interest rate, Singapore is a price taker because we do not control the interest rate in our country.

"Most countries, including the United States and China, adopt an interest rate policy where central banks raise or cut interest rates.

"Singapore is the only major economy in the world to use the exchange rate, guiding the Singdollar higher or lower.

"MAS says the exchange rate is the best tool for a small, open economy like Singapore"

Still, no one can be sure what the longer term picture is going to be but in the shorter term, there will be pain and most of us should be prepared to tighten our belts.

I remember when I paid off my last home loan, my mortgage rate was 5.1%.

Yes, young people might find that rather surreal but it wasn't a bad dream.

It was real.

Interest rates are going higher but no one knows for sure how much higher.

Still, if we are not overleveraged, all else being equal, we should do better than most.

Suddenly, everyone is rushing for the exits and looking for safe harbors to park their money.

So, quickly now, withdraw all our money and stack them up at home (and pray that there are no termites.)

Alamak, I believe in keeping some cash at home for convenience but this is too much lah.

Of course, jokes aside, all of us know about the risk free and volatility free CPF we lucky Singaporeans have.

What about risk free and volatility free Singapore Savings Bonds or SSBs?

Well, long time readers of my blog might remember that I blogged about SSBs donkey years ago.

However, I hardly talk about them compared to how much I talk about the CPF.

I am blogging about the SSB now because many readers left comments about the SSBs in my blog and even my YouTube channel in recent days.

Whether something is good for us or not will depend on what we need and how well it fits that need.

The SSB is designed as another way for risk averse people to save money (up to a maximum of $200K at any one time) for the medium term.

We can tell this is the case because to get the maximum coupon, we have to hold the SSB for the full 10 years.

If our motivation is not to save money for the medium term, then, we have to accept the possibility of receiving smaller coupons if we should make premature redemptions.

The SSB is also safe because there is no penalty for premature redemption although there is a waiting time before we can get our money back.

So, it isn't the nearest of money which means it isn't the best way to store our emergency fund.

An easy solution is to park only a portion of our emergency fund in a SSB if we really want to use it that way.

This might not work if someone has a relatively small emergency fund in which case I think leaving the money in a fixed deposit might be a better idea.

I blogged about this way back in 2015 and if you are interested in what I said back then, read:

Now, having said this, with interest rates rising, if the SSB should offer an average coupon of 4% eventually, it might be a no brainer to park some money in SSBs for the full 10 years as it would mimic the CPF-SA.

It really is not easy to get a consistent 4% risk free and volatility free return especially in a strong currency like the Singapore Dollar.

It is utter mayhem in some markets and things could get worse before they get better.

Who knows?

Things could even get worse for longer if we get stagflation.

Still, as long as we are financially prudent, have a large enough emergency fund and are invested in bona fide income producing assets so that we receive passive income to cover a good portion of our expenses, we should do better than most.

The aim is to be always prepared for winters.

I do not doubt that other than those who are super rich, most of us would have to make adjustments in the event of a longer winter even so.

On 5 May 22, I published a blog on why I was looking to add Bitcoin to my portfolio.

The plan was to have gold, silver and Bitcoin form 4% to 5% of my portfolio as insurance against fiat currencies.

This decision was made after plenty of thinking and research.

Of course, there are plenty of cryptocurrencies available but I am only interested in Bitcoin because of the "Bitcoin is digital gold" line of thought.

I have no interest in the "Buy cryptos to get rich quick" line of thought which has a strong speculative flavor to it.

When something gains traction and greater mainstream acceptance, often, we see variants of it spawning as everyone tries to get a piece of the action.

It is no different in the crypto space and very recently, the crypto space had their version of Blumont/Asiasons crash.

Seeing is believing:

Luna has crashed.

Crash is probably an understatement as this Luna crash puts the craters on the Moon to shame.

Many who placed heavy bets on Luna lost everything.

Terrible.

What about Bitcoin?

Well, it is crashing too but not in such a dramatic fashion.

I only got my little toe in the Bitcoin door a couple of weeks ago.

Why not a foot?

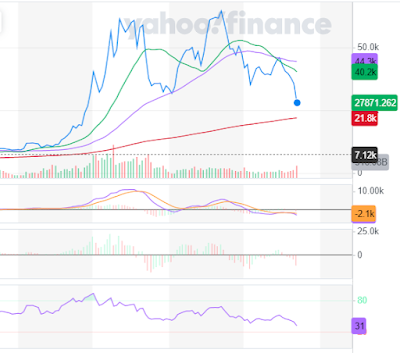

I initiated a very small position because I saw a bear flag in the chart.

The suggestion was that price could go a bit higher and then it could swing lower and I would accumulate only at a lower price.

So, with the price crashing now, when would I be buying more Bitcoin?

Using simple moving averages to throw some light on that matter, the 200 days moving average seems like the one to watch.

Chart dated 12 May 22.

This 200 days moving average is still rising and approaching US$22,000.

Just quick and dirty technical analysis.

Of course, technical analysis shows where the supports and resistance are but it doesn't tell us if they would be tested.

PM Lee recently warned of a possible recession in the quarters ahead.

Put rising interest rate and a slowing economy together, we get a rather gloomy picture.

The evil which is inflation is preferred to the evil which is deflation.

Although inflation is the lesser evil, it isn't as benign when it is heightened which is what we are seeing now in the world.

We can reduce inflationary pressure either by increasing supply of goods and services which are in demand or tempering demand for such goods and services.

As it is difficult to increase supply right away, central banks are trying to tame inflation by increasing interest rate in an effort to reduce demand.

Increasing interest rate increases the cost of debt.

Credit is the lifeblood of commerce and most businesses are leveraged to some degree.

If the economy is healthy, businesses can pass on the higher cost of doing business to their customers and higher finance expense that comes from higher interest rates are naturally a part of such cost.

However, it becomes more difficult for many businesses to pass on such higher costs to customers if the economy is suffering from malaise.

Heightened inflation, rapidly increasing interest rates and low economic growth is not a good mix.

In such a situation, even very strong companies will not be spared a slowdown as most entities would be less ready to part with their money.

Already, we see some big name MNCs both in the old and new economies warning of very difficult quarters ahead.

Only the fittest will survive but even they might not emerge unscathed from such a toxic cocktail.

As an investor for income, I believe that businesses which are able and willing to pay a meaningful dividend should be favored.

To make sure that dividends are sustainable, these businesses should also provide necessary goods and services and have stronger balance sheets.

They too will take a few punches during hard times but they should be able to roll with the punches.

I think staying invested is still the way to go but, like I said, I should mostly be invested in businesses which are able and willing to pay dividends even during hard times.

So, with this in mind, I have taken a hard look at my largest investments since they impact the performance of my portfolio the most.

The strategy to increase my investments in DBS, OCBC and UOB during the COVID-19 induced bear market has turned out well and sticking with this strategy makes sense to me especially with interest rate rising.

I am also interested in increasing my investments in ComfortDelgro and CLCT on weakness as they seemed to have lagged in price recovery while their businesses look more attractive to me in recent times but for different reasons.

I am leaning more towards ComfortDelgro which has a stronger balance sheet and also because looking at the numbers which have improved, there is a fairly good chance that future dividends will be higher and could even go back to pre-pandemic levels.

CLCT's plan is to increase the proportion of new economy assets in their portfolio and I foresee more fund raising in the future.

So, I will increase my investment in CLCT slowly and not bulk up in a hurry.

REITs are required to pay out at least 90% of their operating cash flow to investors to enjoy tax benefits and this is a source of comfort to me.

The REITs in my portfolio are rather conservative when it comes to debt and in the case of IREIT Global, some of their rental income is linked to the German consumer price index and higher inflation could see a greater increase in income.

In my list of largest investments, the only entity which did not pay a dividend during the last bear market was Centurion Corporation.

Amongst my largest investments, Centurion Corporation also has the weakest balance sheet apart from Wilmar International.

However, Wilmar International is in the business of food production and distribution which, in my opinion, is recession proof.

Given their size and market dominance, they should be able to charge higher prices.

Wilmar also has good options available to unlock value for shareholders and they were paying dividends even during the pandemic.

I increased my investment in Centurion Corporation as Singapore decided to live with COVID-19.

For those who are interested in my thoughts on the matter, read:

In an environment of rapidly increasing interest rate and slowing economy, however, with a rather weak balance sheet, it could be harder for Centurion Corporation to bring home the bacon.

In my original blog on why I invested in Centurion Corporation, I crunched some numbers on how rising interest rate could impact Centurion Corporation's interest cover ratio.

Of course, if they are able to increase asking price per bed meaningfully to balance the increase in the cost of debt, then, they should be OK.

Although they would be able to do so easily in a healthy economy, it might not be so easy during times of economic malaise.

Wait, didn't Centurion Corporation do quite well even when the economy was unhealthy?

Yes, they did but they didn't have to deal with rapidly increasing interest rates.

I don't know everything and I might be missing a few things here.

So, I have decided to only reduce my exposure to Centurion Corporation and not go to zero.

As my total passive income held up quite well during the two years when Centurion Corporation suspended dividend payouts, I doubt reducing my investment would have any meaningful impact in terms of passive income generation which makes this decision an easier one for me.

Although Centurion Corporation still looks undervalued to me as it trades at a huge discount to NAV, to be honest, this discount could reduce as valuation of their assets could take a hit.

It would be interesting to see how the management navigates the challenges ahead and how they might unlock value for shareholders.

They are trying to sell some assets in the USA now which if successful should help in reducing leverage and unlocking value.

To this end, I believe they should ramp up their effort and sell more assets.

Like Phua Chu Kang said at the onset of the COVID-19 pandemic, "Things different already."

In the grand scheme of things, this is a relatively minor shift of resources but because I am more inactive than active as an investor for income, it might seem like a big event.

Remember, mentally unstable AK is just talking to himself, as usual.

A couple both age 38 with 2 young children (ages 4 and 6) are thinking whether to sell their fully paid up investment property valued at $3.5m?

If they were to sell the said property, the wife could become a stay at home mom.

The other option is to keep the property and continue to have dual income.

A part of the comment:

I am publishing my reply to this comment as a blog to see what others have to say since I don't have all the answers.

What do I think?

This is my reply:

"Congratulations to this couple because what they have is a first world "problem."

"I cannot provide an answer as to which option is better because it all boils down to what is more important to the couple at this point.

"The choice is not between two evils and to determine which is the lesser evil here.

"The choice is between two outcomes which are good in their own ways.

"Is time spent with the children in their formative years more important or is greater certainty in money making more important?

"What I do know is that kids grow up very fast.

"Growing up, I didn't get to spend much time with my parents as both of them had to work long hours.

"If our family had been financially better off, then, things might have been different.

"Taking the feelings of children into consideration in financial matters is a luxury for most families but for this family, it could be a luxury which is affordable.

"We have to ask how much is enough and I can only speak for myself."

Anyway, it has been many years since I bought more gold and silver.

When I took a look recently, I found that, together, gold and silver formed only 2% of my portfolio.

This is lower than what I think I should have as insurance against fiat currencies.

I was watching some videos on the topic when I stumbled on a video by Robert Kiyosaki who has always said that keeping some gold and silver was sensible.

However, in that particular video, there was a twist because he was also talking about Bitcoin and why we should keep some.

That was very intriguing to me as I don't remember him talking about Bitcoin before.

To be fair, I don't follow him and what I know about him is probably dated.

Like the Dollar, Bitcoin was a currency to me but unlike the Dollar, other than being a digital currency, Bitcoin was not a fiat currency.

Then, while looking for more information, I found a video by Kevin O'Leary who said that institutional investors are looking at Bitcoin not just as a currency but as a property to hold.

So, just like gold, many institutional investors are looking to hold some Bitcoin.

Why?

They believe that Bitcoin is digital gold and, just like gold, Bitcoin is supposed to be a good store of value.

Digital gold for a digital age.

The truth is Bitcoin has gained recognition and a higher level of acceptance.

Fiat currencies are very flawed, after all, and having a crisis mentality and getting some insurance is probably a good idea.

So, I believe we need some insurance for this which is why I hold some gold and silver.

Just like how I stepped out of my comfort zone this year when I got some exposure to Chinese tech stocks, I decided to step out of my comfort zone once more to get some Bitcoin.

Why not simply get more gold and silver?

I could do that but, like I said earlier, digital gold is for a digital age.

I don't know what the future will bring but I really like "Sword Art Online" and "Log Horizon."

Is the Metaverse all hype or would it become mainstream?

I don't know.

I made the decision to get some Bitcoin some time after I decided to get some exposure to Chinese tech and both decisions surprised me for a short while.

Why a short while?

Well, considering that the prices of Chinese tech stocks and Bitcoin had already plunged significantly, maybe, it wasn't so surprising that I got interested when I did.

Anyway, the plan was to have Bitcoin make up 2% to 3% of my portfolio.

Then, together, gold, silver and Bitcoin would form 4% to 5% of my portfolio.

Ray Dalio's perspective on having a small percentage of our portfolio in Bitcoin for the sake of diversification resonates with me:

Still, I have only bought a tiny bit of Bitcoin so far and it isn't even 0.5% of my portfolio yet.

Why did I not buy more?

To invest in Chinese tech was to invest in undervalued productive assets and I nibbled even though price was down trending.

It was just to get a foot in the door.

In comparison, I cannot tell if Bitcoin is undervalued nor is Bitcoin a productive asset.

Bitcoin is just like gold and silver.

Alamak!

How like that?

All I have to depend on is technical analysis.

Very dangerous for me as I am probably somewhat rusty and could get tetanus from the exercise.

Anyway, I am in no hurry to have Bitcoin form 2% to 3% of my portfolio.

I will take my time.

Bitcoin's price is very volatile and big price swings are pretty normal.

Looking at the chart, I see what is possibly a bear flag, Bitcoin could go higher before plunging again in price.

So, after getting my smallest toe in the door earlier in the week, I will pace myself and accumulate whenever price swings lower.

I might get some Etherium too as that's the runner up to Bitcoin in terms of market cap so that I wouldn't be putting all the eggs in one basket.

However, Etherium is not exactly digital gold and, so, exposure to Etherium should be relatively small.

What about Litecoin?

Litecoin is digital silver like Bitcoin is digital gold.

However, buying Litecoin using Gemini, the crypto exchange I signed up with, requires me to use Bitcoin to do so.

So, to avoid paying more commission, I will mostly stick to Bitcoin.

OK, back to the present.

Drumroll, please.

I have done it!

I am a newly minted holder of Bitcoin.

2022 is turning out to be a year of surprises on a personal level.

Like I said, after my initial tiny purchase, the strategy is to accumulate mainly Bitcoin whenever its price weakens.

With this strategy, if Bitcoin weakens in price, I buy more and if Bitcoin appreciates in price, it means I wouldn't have to buy as much to have it hit 2% to 3% of my portfolio.

So, whichever direction Bitcoin goes, I am good with it.

OK, long time readers know I believe in keeping an emergency fund.

Emergency fund is in a chest labelled: "CODE BLUE!"

Bloggy Award

Bloggy Award

{kind=link}