Ever since the CPFB introduced a colorful pie chart of our CPF savings a few years ago, I would look forward to mine every year like a teena...

Past blog posts now load week by week. The old style created a problem for some as the system would load 50 blog posts each time. Hope the new style is better. Search archives in box below.

So, the Fed has increased interest rate by 0.25% and Mr. Market likes it.

Tech stocks are higher and even Bitcoin is higher.

It is not surprising as these are assets which thrive on lower credit cost.

Wait.

Did you say lower credit cost?

But the Fed is not lowering interest rate.

They are still increasing interest rate.

Less steeply, for sure, but still an increase.

Well, you know what they say about Mr. Market being forward looking by 6 months to 9 months?

It could be that Mr. Market thinks that the Fed will reduce interest rates towards the end of the year.

Alamak.

How like that?

Throw all our money including the kitchen sink into tech stocks and Bitcoin now?

Well, I am sure some will do that.

I remind myself that joining Mr. Market's exuberance party could end badly and for those who were bitten before, they would probably be rather shy now.

Anecdotal evidence shows plenty of interest in quality fixed income.

If we can get around 4% p.a. yield from risk free and volatility free bonds and fixed deposits, as investors for income, there is really no reason to put money in tech stocks which pay little or no dividends.

Apple is a tech stock that is all about growth but I wonder if it can continue growing as much as it grew in the past and what is its dividend yield even at the current price?

1%?

What about Tesla?

You mean the company run by the arguably manic Elon Musk who sold billions of dollars of its stock to buy Twitter which he then went on to steer towards the verge of bankruptcy?

Elon Musk threw Tesla's common shareholders under the bus was what AK said to himself.

I am not telling anyone not to buy stocks of Apple or Tesla.

I am just reminding myself why I am not a fan.

Having said this, just like my take on Hang Seng Tech ETF, I think these tech stocks are probably pretty good for trading.

So, for anyone who has the inclination, they could make a bit of money trading these stocks as volatility is the friend of a skillful trader.

The more important word here is "skillful" and not "trader."

(Hint, hint, nudge, nudge, wink, wink.)

Having said this, I have to confess that a slowing down of the Fed's rate increase is a good thing for my "tech-less" investment portfolio too.

Why?

It is good for the REITs, of course.

So, REITs are the same as tech stocks lah, some readers might think.

Well, same same but different.

REITs generate income and share income with their investors.

REITs don't care about growth at any cost, especially not burning money in an effort to grow.

(Looking at GRAB and SEA sideways.)

Having said this, REITs can deal with higher interest rates as long as they are not sky high.

Younger readers might think that the current interest rates are sky high but they are really not that high.

I think interest rates have normalized which isn't a bad thing as money should not be free or almost free anyway.

Cheap money encourages reckless behavior.

More people would benefit from having a greater degree of financial prudence and a higher interest rate is like the cane that stands ready to whack bad actors.

Oh, no, I am rambling again.

Let me wrap this up.

I remind myself to stay grounded.

Higher interest rate is a good tailwind for our local lenders which is good for me.

Slowing interest rate hike is good news for REITs which is good for me.

Interest rate is not being reduced but remains high which is a reminder to stay financially prudent.

Higher interest rate is good for savers and if we are prudent, we are saving money which means higher interest income (which is good for me.)

Yes, the current environment rewards the financially prudent better than before.

It isn't all doom and gloom.

I recently produced a YouTube video on this:

Now, I will try to learn from Mr. Market a bit.

If I try looking forward, if the Fed should stop increasing interest rate after another one or two hikes of 0.25%, I think we could see yields fall.

This is because Mr. Market might rush in to secure the highest possible yield and with greater demand, bond prices go up and yield goes down.

In such an instance, I might resume voluntary contributions to my CPF account which pays an average of 3% p.a. in my case.

This month's Singapore Savings Bond's 10 year average yield is 2.9% p.a. which is a no go for me.

Wondering why this blog sounds a bit off?

It is because I had a nightmare, woke up very early and couldn't get back to sleep.

Still sleepy but I have to go to the hospital later for a check up.

I don't like going to the banks, if I can help it.

So, all the birthday and CNY red packets I received from family members and also money people paid me whenever I helped them buy stuff just got stashed in a drawer.

Today, I opened that said drawer to "deposit" my CNY red packets and I just thought of taking a tally.

OMG!

I have more than $10K in cash stashed away.

With interest rates so high now, I could possibly get $400 in interest payment if I were to place the money in a 1 year fixed deposit which pays 4% p.a.

$400 can sustain my lifestyle for a week easily!

I know OCBC is offering 4.08% p.a. for 8 months FD but they need a minimum of $20K placement.

Not enough.

CIMB only needs a minimum of $10K for their FD promotion.

So, I checked CIMB for the latest rates, being the first day of a new month.

OMG!

CIMB's promo rates have reduced drastically!

6 months FD now pays 3.7% p.a. instead of 4% p.a.

12 months FD now pays 3.5% p.a. instead of 4.2% p.a.

Sadness.

How like that?

What is a retiree like me to do?

I decided to "tikam" 6 months T-bill instead.

Hope to get a cut-off yield of at least 3.9% p.a.

Will try $5K for the T-bill closing today and another $5K for the T-bill closing on the 15th.

If you are new to my blog and wondering if you should do the same, please take note that I am doing this because I already have a significant exposure to equities.

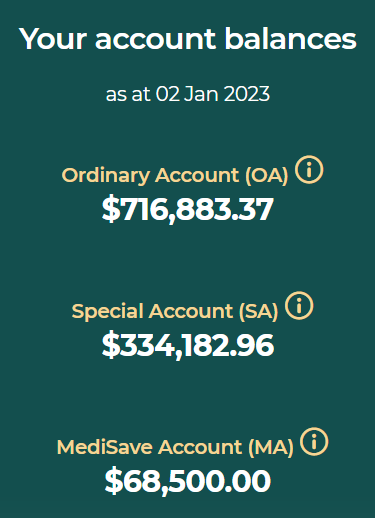

On 5 Jan 23, in what has become an annual activity, I shared my CPF numbers here in ASSI.

After topping up the CPF-MA, this was the picture:

As I grow older, I sleep less.

I wake up earlier and earlier in the mornings.

Most of the time, I just follow a routine in the early mornings but sometimes I do things which are not routine.

Checking my CPF account is not routine.

Yes, despite what some people might think, AK is not obsessed with his CPF account.

At least I think I am not obsessed but I am mental.

You know what they say about crazy people?

Crazy people don't know they are crazy.

Ahem.

When I logged into my CPF account today which I do from time to time because it gives me a sense of security which helps my mental condition, I got an anxiety attack!

No peace of mind?

Why like that?

This was what I saw:

OMG!

Where did my CPF money go?

Did my CPF account get hacked?

Alamak!

Cham liao lah!

Quick, call CPF Board but they not open yet.

Too early in the day.

How like that?

Make police report first?

Then, through the morning mind fog, I recalled what happened.

Sigh.

I used CPF-OA money to apply for the 1 year T-bill.

Crazy AK, seven early eight early, scaring himself like that.

Long time regular readers of my blog might remember that I like saying the government is working hard to help partially fund our retirement.

If we want the government to work even harder for us, make sure we hit the prevailing Full Retirement Sum (FRS) in the CPF-SA and also the Basic Healthcare Sum (BHS) in the CPF-MA as soon as possible.

The magic of compounding is even more magical given a larger base and longer time for it to work.

The CPF-SA and CPF-MA enjoy a floor rate of 4% per annum which, even in today's environment of higher interest rates, is still very attractive.

The CPF-OA, of course, has a floor rate of "only" 2.5% p.a. which until a few months ago was also very attractive.

Money in the CPF-OA was also working hard but only not as hard as money in the CPF-SA or CPF-MA.

It is like working for a company that has a chain of stores and being sent to a store which is still profitable but has the least amount of business in the chain.

Alamak.

What is AK saying?

Spouting nonsense again.

Dementia.

Cham liao.

Anyway, I applied for the 1 year T-bill with CPF-OA money last week and I have been feeling apprehensive ever since.

This is just a bit lower than the 4% p.a. I had assumed in an earlier blog in my calculations.

It is very slightly lower than 3.9% p.a. which was what I thought would be good enough as that would be pretty close to 4% p.a. which is the floor rate of the CPF-SA and CPF-MA.

For a principal sum of $200K, the difference between 4% p.a. and 3.87% p.a. in terms of interest earned (or not earned) is $260.

What about twice or thrice that amount like I mentioned in my earlier blog on the subject?

The difference would be $520 and $780, respectively.

I think most would agree that it is not a tragedy.

A cut-off yield of 3.87% p.a. is not bad especially when we are being paid the "coupon" immediately instead of having to wait 12 months for it.

OK, the feeling of apprehension has evaporated.

I can rest easy again.

So, it seems that a vast majority of my CPF-OA money is leaving home for the first time ever.

Like a proud parent sending off his children to a prestigious overseas university, I know my CPF-OA money will return stronger after spending 1 year in T-bill university.

Next up is a 6 months T-bill with its auction on 2nd February and I will be using cash on hand to make the application.

As long as yield hovers at around the current level, I am going to keep buying T-bills.

Hopefully, I will have the resources to do so every two weeks.

If things don't go awry, I would like to keep doing this until April when money from the first T-bill I bought in October last year returns.

It would just be recycling returning funds from then on.

I am aware that some banks like CIMB offer 4% per annum interest rate on 6 months fixed deposits.

However, I only think of DBS, OCBC and UOB as being somewhat on par with T-bills in terms of being relatively risk free if we should have $75K or more in deposits.

Unfortunately, our three local lenders are rather parsimonious.

What to do?

Look out for better fixed deposit promotions from our local lenders!

Currently, DBS has a 3.9% p.a. 5 months fixed deposit promotion for a minimum of $20,000 placed.

The banks are in a good place to enjoy a strong tailwind provided by rising interest rates.

Even in a recession, the banks should continue to bring home the bacon as they are well capitalized and should have no problem paying dividends.

Nothing was sacrosanct in the reallocation exercise and several very small positions in my portfolio were closed down while some larger positions were reduced in size.

Apart from OCBC and UOB, I could not resist increasing the size of my investment in IREIT Global as the fundamentals remain sound and the REIT's unit price hit what I felt to be distressed levels.

It would be impossible to buy any asset owned by IREIT Global at about 40% discount to valuation but we could if we bought some of IREIT Global from mid 3Q to 4Q 2022.

To be fair, that 40% discount to valuation could reduce somewhat as the REIT is going to take some time to backfill the space at Darmstadt vacated by Deutsche Telekom.

The valuation of that particular property could come under pressure, therefore.

However, if we are investing in properties for the longer term and we should be, it isn't a tragedy that it might take some time to see results as the space will be leased out eventually.

IREIT Global has the most defensive financials I can find amongst the REITs which I own while offering a distribution yield of around 8%.

With the accumulation of IREIT Global in 4Q 2022, it is my largest investment in the S-REIT universe today.

I also added to my investment in Wilmar International as the business became more profitable in spite of a challenging environment.

In the worst case scenario where we see stagflation, I have an inkling that Wilmar International could outperform as the world faces a food crisis.

I nibbled at LION-OCBC Hang Seng Tech ETF as it overshot the low formed on 15 March 2022 but like I said in an earlier blog, it would likely be the last time I added to my position in the ETF as I am not too keen on trading regularly in order to make money.

Too lazy.

I did subsequently reduce exposure when the unit price rebounded in November.

I reduced exposure again in early December as the ETF's unit price rose to test resistance provided by the descending 200 days moving average which was approximately at 71c:

Those couple of trades produced a capital gain of around 23% and reminded me of why I spent so much time trading the stock market many years ago.

Some readers might remember that I shared in my blog as well as during one or two "Evening with AK and friends" that I made around half a million dollars in my adventures as a stock trader many years ago.

Trading stocks could be financially more rewarding than investing for income but it requires more activity and some knowledge of technical analysis.

I have decided to become more laid back in recent years to spend time on other things in life.

Anyway, the average price for my remaining position in the ETF is probably low enough to make Chinese tech stocks look cheap even to value investors.

A simple reversion to mean would result in a capital gain for me.

I do not need to see euphoria and the ridiculously high valuations when the market was sloshing with almost free money in order to have a good result here.

However, it is a tiny position in my portfolio and it would not move the needle much.

In bonds, I have put money earmarked for contribution to my CPF account into Singapore Savings Bonds (SSBs) while money from maturing fixed deposits went into Singapore Treasury Bills as yields of these government bonds reached levels which I found to be more attractive.

The changes made in 4Q 2022 to my investment portfolio is consistent with what I have said many times before and that is not to be overly optimistic nor overly pessimistic but to stay pragmatic.

Having a percentage of my portfolio in fixed income like SSBs and Treasury Bills now while staying invested in equities which I feel will likely outperform fixed income (including my CPF savings) in the longer term should result in a more resilient investment portfolio.

If I feel that equities would outperform in the longer term, why am I still putting money in fixed income?

It is about having peace of mind as an investor.

Fixed income instruments are important for investors who cannot afford or at least feel that they cannot afford to be too adventurous as fixed income helps in reducing the volatility in our portfolio.

Not everyone is able to stomach greater volatility, whether it is due to a lack of financial ability or mental strength to do so.

Now that yields are reasonably attractive, they also help to reduce the cost of insurance that is the opportunity cost of not getting possibly higher returns.

There were times when I was very adventurous as an investor and I was fortunate to be well rewarded many times but I also suffered losses sometime.

The emotional roller coaster that came with being more adventurous wasn't a lot of fun either.

Anxiety and depression are only interesting topics to psychiatrists.

Having said this, I am also partial to fixed deposits which offer relatively high interest rates as I continue to maintain a meaningful cash position which is mostly my emergency fund and float.

This cash position has helped to keep me sane during bad times and it still does.

What about the opportunity cost of not being invested?

There isn't much left in my war chest as the funds have been substantially deployed.

Well, regular readers would have an inkling that there wasn't much in my war chest to begin with as I lack an earned income and consume most of my passive income.

Even the government takes pity on me and gives me money every year.

Anyway, enough of self pity.

So, how much passive income did my portfolio generate in 4Q 2022?

S$ 25,331.81

It is a relatively small sum compared to passive income in 3Q 2022.

However, to put things in perspective, 4Q 2021's passive income was:

S$ 21,283.82

So, year on year, 4Q 2022's passive income came in 19% higher.

Looks more impressive percentage wise but I get it that the dollar value increase is smaller compared to 3Q 2022 which saw a smaller percentage increase at less than 10% improvement, year on year.

4Q 2022 passive income includes income received from 6 months Treasury Bills which I started buying only in October.

This new passive income component is a relatively small trickle but every little bit helps.

My passive income for the whole of 2022 is:

S$205,999.73

This is almost 20% higher when compared with S$171,854.30 generated in 2021.

Average passive income per month in 2022 was about:

S$17,166 per month.

Can't really complain.

I am contented.

Now, I ask an important question.

What is 2023 going to be like?

It is more likely than not that recession is coming to many parts of the world even as we get used to the idea that higher inflation is going to stay with us for some time to come.

So, with inflation high and economic growth evaporating thanks in part to rapidly rising interest rates, we could also see stagflation.

Therefore, I would be quite happy if my passive income in 2023 is similar to 2022, give or take a few percentage points.

Not going to raise the bar as I could be disappointed.

What else am I telling myself?

As an investor for income, I cannot dictate how much my companies should pay me but I can certainly tell myself how to spend my money.

What to do?

Will have to tighten my belt.

Buckle up for a bumpy ride.

Don't throw caution to the wind.

Hold on tight to our emergency funds for dear life!

I continue to remind myself that fixed income investments are more attractive than before.

Having a meaningful percentage of risk free and volatility free T-bills and SSBs in my portfolio is not a bad idea.

The CPF might not be as sexy a "fixed income" instrument but it isn't wrong to keep thinking of it as an investment grade bond with a significant annuity angle.

The CPF still works as a risk free and volatility free investment grade sovereign bond which helps to provide a greater degree of certainty when it comes to retirement funding.

These fixed income options help to form the large base of my investment pyramid.

I also remind myself the importance of staying invested in bona fide income generating businesses which generate meaningful and sustainable income for us.

Getting rich slowly isn't as sexy as getting rich quickly but like I said before, the journey to financial freedom is not a race: HERE.

In summary, for regular folks, don't be too adventurous as having strong and reliable cashflow is important.

To be clear, it has always been important but with heightened rising costs in so many forms and much greater economic uncertainty, it is probably more important than ever.

Focusing on our portfolio's ability to generate income and not our portfolio's market value (now or in the future) might not be a bad idea.

Remember, I prefaced these highlighted paragraphs with the words "for regular folks."

If you are a very rich or "jin satki" person, it might not apply to you.

If you are not very rich or "jin satki" but act like you are, good luck to you.

Very rich people can take a few hard knocks and still survive.

For example, they could lose a few hundred thousand dollars or more in Tesla or Alibaba but still stay rich.

Those who are not very rich might find themselves in financial distress especially if they had borrowed money to do the same.

Peace of mind is priceless.

2023 is likely to be a relatively difficult year for most regular folks.

Stiff upper lip and stay the course.

As long as we are moving in the right direction, we should make incremental improvement and move towards financial freedom.

Bloggy Award

Bloggy Award