Ever since the CPFB introduced a colorful pie chart of our CPF savings a few years ago, I would look forward to mine every year like a teena...

Past blog posts now load week by week. The old style created a problem for some as the system would load 50 blog posts each time. Hope the new style is better. Search archives in box below.

I have been watching lots of videos on YouTube lately and learning new stuff.

I have also been watching more Chinese drama and anime lately.

My goodness, the Chinese have some high quality stuff!

All this happened while I was researching Chinese tech stocks before deciding to get some exposure.

Had to sacrifice some gaming time, unfortunately.

Genshin Impact is so good and it is Chinese too!

Now, I only log in to do my dailies, run a few domains and take part in events.

I still log in to Neverwinter daily to collect my rewards and run some dailies.

All in all, gaming takes about 2 hours per day max.

I have said before that I cannot imagine being bored in retirement and that is still true.

There is just so much for me to do.

Anyway, yesterday, I took a look at my own YouTube channel.

AK has a YouTube channel?

Yes, indeed, long time readers might remember my YouTube channel which I started more than 11 years ago in October 2010.

Surprised?

I have forgotten how long ago it was and I was surprised when I looked at the date of my first video.

I started blogging in 2009 on Christmas Eve out of curiosity and boredom.

Blogging has been an amazing outlet for me to talk to myself.

No regrets.

I started my YouTube channel for mostly the same reasons.

Feeling nostalgic as I watched my own YouTube videos, I thought I would do a quick blog to share the old antique with anyone who might be feeling bored and curious like I was when I started the channel.

I published a blog a few days ago on Lion-OCBC Securities Hang Seng Tech ETF and how I was using it to gain exposure to Alibaba, Tencent and some other Chinese tech companies.

I said that I was taking it slow with the ETF and that my initial investment wasn't even 0.5% of my portfolio in market value.

Why take it slow?

Although there were some signs that the dust could be settling, technically, the downtrend was clearly still intact and low could go lower.

Buying the dips in an uptrend would be buying as Mr. Market climbs a wall of worries but in a downtrend, Mr. Market flows down a river of hope.

Getting our hopes up in a downtrend could set us up for disappointment.

Also, most of the time when I went wandering out of my circle of competence in the past, I ended up hurting myself and pretty badly sometimes too.

Although I researched the ETF and some of the Chinese tech companies it was tracking before I made the decision to put some money on the table, I was very sure I only scratched the surface.

Anyway, consistent with my plan to limit exposure to 1% of my portfolio for a start, I nibbled at the ETF earlier today at a price 10% lower than my initial investment.

With this purchase, my total exposure to the ETF stands at around 0.5% of my portfolio now.

What do I plan to do next?

I will be waiting to see if the low of 15 March would be tested in the coming weeks.

If the low should be tested, I would most likely double my investment to increase total exposure to around 1% but I might add more if I should see a positive divergence.

I would look at the momentum oscillators like the MACD and RSI to do this.

Positive divergence means higher lows in the momentum oscillators as price retests the low or forms a lower low.

A positive divergence would give me the signal to add more to my investment.

It would suggest that the selling pressure could be easing and that the price could see a more sustained recovery.

Still, I would take it slow because we could also see lower lows in price and higher lows in the momentum oscillators for many months to come.

In the absence of a positive divergence, I would err on the side of caution and not add too much to my investment.

It is no secret that I spend a lot of my time gaming online.

I have also been buying lots of things online.

I hardly leave my home and, so, I have become even more of a hermit in recent years.

Anyway, with my lifestyle, shouldn't I be interested in Alibaba and Tencent?

Well, on top of them being Chinese, as a retiree who depends on passive income for a living, I find it harder to be interested in them.

However, I am a relatively young retiree.

So, maybe, same same but different.

I have given it a lot of thought recently and I have decided that I should be at least a little bit interested in having some exposure to Alibaba and Tencent with their prices being where they are.

Not too much exposure though.

Just like adding some black pepper to my soup, powdering my portfolio with some Alibaba and Tencent to give it some pizzazz might not be a bad idea.

Invest in Alibaba because it is the big brother when it comes to online shopping platforms.

Invest in Tencent because it is the big brother when it comes to developing online games.

Of course, they do more than these but I am too lazy to list everything they do.

It is easy to find the information online and anyone who is interested can do a simple search.

Both Alibaba and Tencent are inexpensive for tech stocks if we look at their financial ratios.

Still, cheap could stay cheap as long as Mr. Market lacks confidence or interest in them.

I have not invested in any Chinese companies since China Minzhong donkey years ago.

China Minzhong had a PE ratio of only 3, if I remember correctly.

Chinese banks also look relatively cheap and they pay dividends too.

I think you get the idea.

In one of my blogs on Alibaba, I said:

"I waited for the dust to settle during the last bear market and for share prices to find a bottom before increasing my investment in the local banks.

"If I were interested in investing in Alibaba, I would do the same."

So, since I have decided that I am interested in Alibaba and Tencent, has the dust settled?

Well, it does look like their prices have "bottomed" in the middle of March, recovered and are now consolidating.

It doesn't mean that prices cannot move lower.

We could even see a retest of the "bottom" formed in March.

I say "bottom" because we wouldn't know that it is the bottom until the downtrend reverses for sure.

Yes, if we zoom out and look at the big picture, the downtrend is still very much intact.

So, for now, we can say prices have found a floor as we cannot be sure they have bottomed.

A floor with a big plunge pool, maybe.

Plunge pool.

Ooh.

Sounds so exciting.

So exciting that some people got a heart attack.

Then, what about double or triple plunge pools?

Alamak, liddat how?

Looking at the moving averages, Alibaba and Tencent are still stuck in a downtrend.

However, if prices were to retest the lows of 15 March, we would probably see strong buying interest.

People who missed the fun of playing in the first plunge pool wouldn't want to miss the fun again.

It is just market psychology at work.

If the buying pressure is strong enough, we could then see a double bottom forming.

Of course, we wouldn't know a double bottom has formed until the trend reverses for sure.

Yes, technical analysis can be pretty irritating.

Although I am interested in Alibaba and Tencent, I am not interested in buying their stocks in HK or the USA.

Why?

AK is lazy.

AK doesn't like "mafan" stuff.

I want to keep things simple and, so, I have decided to gain exposure through an ETF in Singapore, specifically, the Lion-OCBC Securities Hang Seng Tech ETF.

I have hyperlinked the name to the ETF's website to make it easy for interested readers to find out more about the ETF.

Eh, lazy AK not so lazy after all?

No lah.

I was reading about the ETF and have yet to close the tab to the website.

So, might as well.

Don't spoil my reputation for being lazy hor. ;p

The ETF is listed on the SGX and I don't have to worry about exchange rates, having a custodian account in another country and paying a custodian fee for each counter invested.

The ETF also has the advantage of being diversified and would give me exposure to some other Chinese businesses that I know like Lenovo, JD.com and Xiaomi too.

There is a management fee as there will be some expenses but they aren't sky high.

Yes, I am not as tight fisted with money as I once was and I feel that the fee is a small price to pay for the convenience.

Having things easier for me promotes peace of mind which is priceless.

So, maybe, this ETF is better for my heart in more ways than one.

This ETF is about growth and does not pay a dividend.

Consistent with my asset allocation pyramid, investments which are purely for growth will together form a much smaller percentage of my entire portfolio.

S = speculative positions.

Since I don't have any investment that is purely for growth other than this ETF for now, I could possibly put more money into it if the unit price plunges again (and again.)

Even so, the ETF should still form a very small percentage of my portfolio, all else being equal.

Maybe, just 1% of my portfolio for a start and I feel a 5% cap is probably a good idea.

As it now stands, I still have some way to go before it gets to 1%.

Yes, I being very cautious on this adventure.

Like with all adventures, no matter how well prepared we are, we must be mentally prepared for the worst while we hope for the best.

Some people compare Alibaba and Tencent to Amazon, for example, and if they are right, we could see a fivefold or even tenfold return in the next decade or two.

If this happens, then, even at 1% of my portfolio, in absolute dollar terms, it would be pretty amazing.

So, how likely is this?

To be honest, I would be quite happy if the investment sees a threefold increase in market value in the next decade.

Some might say I am being pessimistic.

Alamak, if I am pessimistic, I wouldn't have put down any money.

Long time readers might remember that I said on many occasions that we want to stay pragmatic and not be optimistic nor pessimistic.

Easy to say, of course.

Getting some exposure to Chinese tech at this point is me trying to be pragmatic.

It is so much fun to make predictions but I remind myself of some facts to stay grounded.

China is not the USA.

The USA, for example, does not care about "common prosperity."

Anyway, unless coming out of retirement and rejoining the workforce is something I am willing to consider, I shouldn't be too adventurous when it comes to investments.

This ETF is probably not a good fit for anyone who is a purist investor for income.

It is probably not a good fit for anyone who does not have the stomach for price volatility either.

QAF was one of my largest investments by market value at one point although it was a rather small largest investment like my investment in Sabana REIT is today.

So, when was QAF one of my largest investments by market value?

It was back in 2017 when it was trading at more than $1.40 a share.

As I believed QAF was worth much more, I added to my investment back then, averaging up.

The highest price I paid was $1.42 a share.

Regular readers know I don't usually bother to calculate average prices of my positions since as an investor for income, my favorite holding period is forever and average prices aren't very meaningful to me.

As long as I feel that I have paid a fair price, it is good enough for me.

However, for this blog, I decided to calculate the average price because it would help to show how investing in bona fide income producing assets which pay meaningful dividends is less problematic even if we have paid a higher price.

My average price after averaging up was about $1.02 a share which meant that I have been nursing a paper loss since then although if I were to take into consideration the dividends received, not too bad.

The longer I stay invested, the safer it becomes.

Averaging up isn't always wrong but, of course, Mr. Market is always right.

So, through this lens, I was wrong to average up in this case.

Very cham liddat. (TmT)

Of course, regular readers know that during the COVID-19 induced bear market, I was adding to some of my investments as the dust started to settle.

Most of my war chest went to investing in the local banks and IREIT Global.

Then, later on, after the dust settled, Sabana REIT.

I had a list of businesses I would have liked to significantly increase exposure to but I didn't have unlimited firepower although I did manage to nibble at some of them.

I had to prioritize those businesses which I thought were more interesting.

The purchases involving UOB, IREIT Global and Sabana REIT were all six figure sums and were relatively large by my standards.

Mostly exhausted after those purchases, my war chest needed time to recover.

With a bigger cash pile in 2022, I decided to add to my investment in Centurion Corporation towards the end of 1Q as its stock price languished.

Then, looking around more recently, I decided to add to my investment in QAF Limited.

Back in 2021, QAF was already trading at 90c to $1 a share.

Yes, I should have bought some in 1H 2020 but hindsight is, of course, perfect and mostly useless.

Anyway, with the price of its stock languishing, I decided to add to my investment quite recently.

QAF's latest numbers shows a much stronger balance sheet which I like.

With a stronger balance sheet, QAF will not have to rely on debt too much to grow organically.

I continue to believe that QAF is a business that is recession proof and it could even benefit from an inflationary environment.

Inflation is, of course, a hot topic.

QAF had a difficult 2021 and with higher prices of wheat and energy likely to be persistent in 2022, it is easy to understand why Mr. Market is feeling somewhat pessimistic.

However, looking forward, QAF should eventually be able to pass on the increase in business costs to consumers as demand for its products should be relatively inelastic and demand could even strengthen during hard times.

Of course, I say "eventually" because if inflationary pressure should strengthen too much too quickly, things could get hairy in the shorter term.

Still, I doubt most people would stop buying their favorite loaf of quality bread just because the price has gone up by 20 or 30 cents or even a dollar.

In fact, I paid a higher price for my loaf of Gardenia low GI soft grain bread today.

Anyway, is QAF one of my largest investments now?

Even after recently adding to my investment, unless its share price goes back to $1.40 or so a share, QAF is still one of my larger smaller investments.

Of course, I could add more aggressively to my investment in QAF and make it one of my largest investments now.

However, with a war chest that is still recovering from big purchases in the last bear market, I think pacing myself is probably a good idea.

My war chest, after all, is not growing as quickly as it was able to when I was still gainfully employed so many years ago as much of my passive income is used to meet financial obligations in my retirement.

My bowling ball that sometimes cosplays as a crystal ball agrees.

ComfortDelgro is the weakest position in this bracket no thanks to the pandemic but even with the huge decline in its share price, the market value of my investment is still above $200,000.

Centurion Corporation is a much larger investment for me today and it is close to being promoted to the next bracket.

I blogged about Centurion Corporation recently and if you don't remember, see: 1Q 2022 passive income.

Like ComfortDelgro, I expect things to improve from here for Centurion Corporation.

UOB is a new member in this bracket as I only became invested in the bank during the last bear market.

My investments in DBS, OCBC and UOB are very close to being promoted to the next bracket as their market values have ballooned.

I have not added to my positions since the last bear market.

So, this is mostly due to the higher prices of their common stock.

To reduce my reliance on REITs for income, building long positions in all three local banks has proven to be rewarding thus far and I hope it continues to be so.

I just watched a YT video on the "lying flat" movement that originated in China.

What is this?

"Tang ping (Chinese: 躺平; pinyin: tǎng píng; lit. 'lying flat') is a... movement in China beginning in April 2021. It is a rejection of societal pressures to overwork , such as in the 996 working hour system..."

996 means working from 9AM to 9PM for 6 days every week.

Apparently, the movement has even moved to the USA which is partly why it is harder for American businesses to find workers now which contributes to inflationary pressure as well.

"Lying flat" is different from achieving financial freedom.

It is about living a very low maintenance life to make our money last for as long as possible without having to work and then going back to work when we have run out of money.

Then, go back to "lying flat" until our money runs out and then going back to work for some money.

Many things boggle my mind these days but this idea of "lying flat" takes the cake.

Some readers might remember that someone said that financially free AK should be ashamed of himself.

As the world continues to grapple with variants of COVID-19 with the latest being the Deltacron or the offspring of the Delta and Omicron variants, Russia decided to start a war.

Inflation which was already gaining steam was pushed higher.

The Fed increased interest rate and there will be more to come.

In an inflationary environment, we will see rising prices in commodities and we could see companies like Wilmar doing better.

In an environment of rising interest rates, we could see banks doing better.

Even REITs could do better and for those who missed my latest blogs on REITs, see:

For those who are well read, guess where this passage came from?

Anyway, regular readers know that I didn't do much in the stock market last year.

I feel that, overall, my investment portfolio is in pretty good shape.

None of my investments which matters to me is keeping me up at night.

(Only Genshin Impact keeps me up at night now.)

Last year, I added to my investment in Sabana REIT in early 2021 and then added to my investment in Wilmar as its stock price sank in 3Q 2021.

Nothing else.

So, I didn't do much last year but what about this year so far?

Well, I thought I wouldn't be doing anything in 1Q 2022 because I rather liked how my investment portfolio looked.

As I did not buy much of anything in the stock market in more than a year, my cash pile has been growing at a steady pace which really isn't a bad thing.

However, towards the end of 1Q 2022, I decided to add to my investment in Centurion Corp.

My investment in Centurion Corp. was already very substantial and I really shouldn't be adding but I just couldn't resist it.

So, I guess AK doesn't have as much character as he thought he had. (TmT)

There is only a small handful of people who each has 1 million or more shares of Centurion Corp. and if I am not careful, I might join their ranks.

Prior to 1Q 2022, the last time I added to my investment in Centurion Corp. was in 2020.

I should say "the last few times" because looking at my records, there were multiple entries made at 32c a share in 2020.

Why couldn't I resist adding to my investment?

OK, I had a chat with my bowling ball and it had a few things to tell me.

Centurion Corp. has weathered the pandemic well and has stayed profitable despite the challenges.

This speaks volumes.

Well managed and resilient, Centurion Corp. is paying dividend again.

Although it is just 0.5 cent per share, my bowling ball told me that they could have easily paid 2 cents per share.

Really?

See:

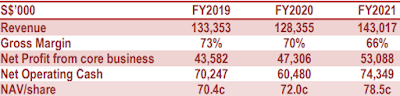

If we look at the numbers, net operating cash not only recovered but exceeded pre-pandemic level.

Centurion Corp. was paying 2 cents dividend per share prior to the pandemic.

Then, why only 0.5 cent dividend per share now?

My bowling ball was silent on this.

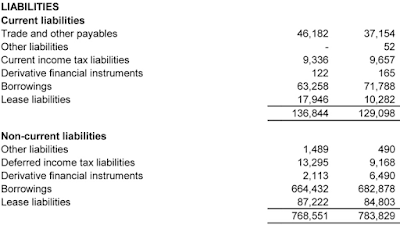

If I were to make a guess, they are probably being cautious which isn't a bad thing, especially if they plan on paying down debt in the face of rising interest rates.

Looking at their financial statement, Centurion Corp. reduced borrowings last year when dividends were suspended.

Of course, if they have identified new businesses which would generate more income but would like to draw on internal resources instead of debt, it isn't a bad idea either.

Centurion Corp. should pay a larger dividend to shareholders if they have no better use for the money on hand.

Centurion Corp. has recovered well and seems to be as valuable a company today as it was pre-pandemic.

In fact, if we look at the NAV/share, it is much higher than it was pre-pandemic which suggests that Centurion Corp. is even more valuable today.

For the rest of the year, we could see Centurion Corp. doing better as Singapore eases border restrictions and more foreign workers return.

While the price of its stock languishes even as things improve, it seems like a good opportunity to increase my investment in Centurion Corp. and at a bigger discount to NAV too.

Centurion Corp. is undervalued but it could stay undervalued for a long time.

It might take a while but I like to think that patience will be rewarded.

"UOB Kay Hian analyst Adrian Loh has kept "buy" on Centurion with a higher target price of 45 cents from 43 cents previously." Source: The EDGE.

Now, time for my passive income numbers.

In 1Q 2022, the three largest income generators for me were:

1. IREIT Global

2. AIMS APAC REIT

3. Sabana REIT

Total passive income received in 1Q 2022:

S$ 40,697.68

In 1Q 2021, my passive income was $36,551.14 and that was some 48% higher than it was in 1Q 2020 due to larger investments made in Sabana REIT and IREIT Global.

So, the fact that 1Q 2022 passive income was some 11% higher than it was in 1Q 2021 makes me very happy and the bigger number is thanks to IREIT Global's stellar performance.

I like investing in good income generating assets.

I like investing in them especially if they are undervalued.

IREIT Global not only generates good income for me, the REIT is also financially strong which gives me peace of mind:

From the numbers, to me, IREIT Global is clearly undervalued.

I have many blogs on IREIT Global and if you are interested, use the Search function at the top of the web version of my blog to find them.

There won't be any income distribution from IREIT Global and Sabana REIT in 2Q 2022 but DBS, OCBC and UOB should be paying dividends then.

It will be interesting to see if my passive income improves year on year in 2Q 2022 as the banks were still paying lower dividends in 2Q 2021.

1Q 2022 was filled with bad news and, for me, passive income was a bright spark amidst all the doom and gloom.

If we hold a relatively diversified investment portfolio of bona fide income producing assets, we should enjoy some peace of mind even as the world seems more than a bit messed up.

Hold some investment grade bonds too and regular readers know that the CPF does that for me.

Bloggy Award

Bloggy Award