Regular readers know that I strongly believe in the CPF system.

I believe that it is a good habit to sock away some money consistently.

In other words, I believe in saving money.

We never know what could go wrong in life and having some savings, substantial savings, is really comforting.

Of course, I also say that we should put our money to work.

We don't want to spend our life working for money.

We want our money to work so that we can enjoy our life more.

So, parking our money in the CPF in an environment of lower interest made good sense as it paid much higher interest rates.

However, in an environment of higher interest rates, to be fair, 2.5% p.a. is pretty decent too.

Still, we would like to have higher returns where possible from instruments with the same risk profile.

This was why I bought a 1 year T-bill with CPF OA funds about one year ago.

Well, the T-bill is maturing today and the money is coming back.

I will perform a transfer from CPF IA to CPF OA when it happens.

Unfortunately, it would not make it back into my CPF OA before the end of the month.

So, I will lose 2 months of additional interest from the CPF OA instead of 1 month.

The breakeven cut-off yield for that T-bill is 2.92% p.a.

For those who are interested in finding out the breakeven cut-off yields, here is a link to a blog that does it: https://growbeansprout.com/cpf-t-bill-sgs-bond-interest-rate

Since that 1 year T-bill had a cut-off yield of 3.87% p.a., I received additional interest of more than $6K.

The funds deployed was almost $700K which explains that more meaningful difference.

Better than leaving the funds inside my CPF OA.

Since I received it as a discount immediately upon the commencement of the T-bill, the interest rate really was higher than 3.87% p.a. compared to a fixed deposit where interest earned is received at the end of the tenure.

I also bought another T-bill with CPF OA funds, leaving only $20K in the CPF OA, and that is maturing in March.

That was a much smaller sum.

Like I said in an earlier blog post, I would place competitive bids using CPF OA funds to buy T-bills.

Non-competitive bids run the risk of getting a cut-off yield that is lower than the breakeven using CPF OA funds.

Since the highest breakeven cut-off yield is 3.33% p.a. which is for 6 months T-bills possibly losing 2 months of additional interest from CPF OA, a sensible competitive bid is 3.5% p.a.

So, that is the plan.

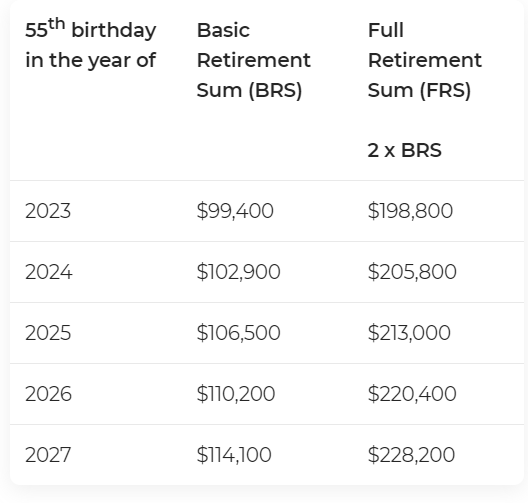

When I turn 55 years old in 2026, after setting aside the Full Retirement Sum in the newly created RA and locking up the Basic Healthcare Sum in the MA, the rest of my CPF savings becomes my emergency fund since I could withdraw the money anytime I want.

That would free up my existing emergency fund which would become part of my war chest.

That would be quite a substantial boost since my current emergency fund is able to cover 24 months of expenses for my parents and myself.

Years of careful planning and patient execution is paying off.

If AK can do it, so can you!

Bloggy Award

Bloggy Award