Recently, I was asked a question on how much do we need for retirement?

It is one of those questions which seem easy to answer but, if we spend more time thinking about it, we realise it is actually not that easy.

I talked about needs and wants in another post earlier.

What are needs and what are wants?

See:

Money management: Needs and wants.

There are certain basic needs in life but there are many wants which have become needs in modern society.

Therefore, how much do we need for retirement could depend on how many wants we have in life, wants which have been internalised as needs over the years.

An important question to ask is, then, what do we need for retirement?

This is a qualitative question and needs to be answered. Otherwise, we cannot start estimating how much do we need for retirement.

So, the person who put the question to me was left scratching his head as I gave him not an answer but another question.

Very often, people wonder how much they need for retirement, wonder if a million dollars is enough or maybe two million dollars.

They should think about what they really need in life and what would they be contented with.

Perhaps, they should not keep chasing after that first million.

Perhaps, they should not keep thinking about how much do they need.

Perhaps, they should think of what they really need instead.

Planning for retirement?

You might want to read these:

1. Inflation adjusted retirement plan.

2. POSB ManuRegular Payout better?

3. Selecting a good financial adviser.

4. OCBC BCIP.

5. POSB INVEST SAVER.

6. A cornerstone in retirement funding.

7. Wealthy nation cannot afford to retire?

FAKE ASSI AK71 IN HWZ.

Featured blog.

1M50 CPF millionaire in 2021!

Ever since the CPFB introduced a colorful pie chart of our CPF savings a few years ago, I would look forward to mine every year like a teena...

"E-book" by AK

Second "e-book".

Another free "e-book".

4th free "e-book".

Financially free and Facebook free!

Subscribe To ASSI

Retirement planning (How much do we need or what do we need?).

Monday, August 9, 2010Courage Marine: Range bound.

Price seems range bound between 19.5c and 18.5c. The BDI has been rather anemic of late and that could perhaps partly account for the lethargy in Courage Marine's share price.

The MFI, OBV and RSI have all recently flatlined. Nothing seems to be happening. In a range bound situation, look at the Stochastics and we see it high in the overbought region. This suggests that price, which happens to be at the upper end of the range identified, could find it hard to move higher for now.

The good news is that MACD has been rising slowly in positive territory above the signal line. The return of positive momentum provides some cheer although we should remember that it is a lagging indicator.

FSL Trust: Where to from here?

An article, Shipping Trusts: A closer look, 13 July 2010, in Next Insight says it well:

I know of at least two blog masters who have liquidated their investments in FSL Trust recently at a loss: Mike Dirnt and Musicwhiz, admitting that their investments were mistakes. JW of Wealthbuch almost put some money in FSL Trust just before the recent crash from 60+ cents based on the posts by Grandmaster89 in an investment forum. Grandmaster89 has become more grounded in his views since. More recently, Alvis of A Investor bought some units at a price close to the bottom at 30+ cents based on TA.

I still have units in FSL Trust bought at $1 in the early days, probably at about the same time Musicwhiz bought his units. I have been thinking of divesting these units but was not as deft as Mike Dirnt to divest at >60c at the recent high; nor did I divest last week like Musicwhiz at a rather much lower price.

I also have some units which I bought in the recent crash. Why? I explained that the purchases were made based on TA and are for a trade. Looking at the charts, FSL Trust's price has not just found a floor, it has most probably bottomed. So, would I sell at the bottom? No.

In fact, the low formed on 11 Jun at 36c would be a strong support if price does decline to that level again. Market participants would remember that price as the low and they could have made some money if they had bought more then. More likely, however, the recent many times tested support at 37.5c would act as an effective breakwater in case of a decline. What about the upside? For now, it seems that the price could remain trapped in between the 20d and 50d MAs for a while. These assumptions are valid as long as everything else in FSL Trust's business remains constant.

From a FA perspective, it is true that FSL Trust has very high risks and its propects seem bleak in the longer term but would it go belly up in the next few months? Rather unlikely as the world economy is still on the mend and the fortunes of the shipping industry are looking up.

Related post:

High yields: Successes, failures and the in betweens.

Charts in brief: 26 Jul 10.

High yielding REITs.

I came across an article which reported Morningstar analyst John Coumarianos saying "I guess people are so exasperated with earning nothing on money market [funds], so they're opting for the 2 to 3 percent [yield] that they're getting on a REIT fund".

This is a reference to the situation in the USA. 2 to 3 percent yield? That's peanuts compared to what we are getting from REITs in Singapore! I mentioned before that a 5 to 6 percent yield in a REIT is not enough to attract me because I can get an almost 10 percent yield in some REITs here. I think investors in REITs here are spoilt!

After the subprime mortgage crisis, all types of real estate investments were punished. Many experts thought that commercial real estate would be the next big bust. "The headlines were all so bad with the housing market," Sorensen says. "REITs don't have a ton to do with the housing market, and expectations there were so depressed. The reality has been better than expected."

Read the article here.

Will the REITs Rally Continue?

Related post:

Create more passive income with limited capital.

Property prices in Japan.

Sunday, August 8, 2010

Property prices in Japan may be near the bottom because transactions are picking up as loan default rates begin to decline....

.... Investors including Chuo Mitsui Trust & Banking Company and CLSA Capital Partners have said they will invest in real estate in Japan this year after the nation’s commercial land prices fell to the lowest in at least 36 years....

.... ‘The best time to invest is before things hit bottom, because if everyone were to agree we are right at bottom, they would all come rushing back in. If you have a longer term outlook, now is a very interesting time to be looking,’ said Buddy Ferrie, a general manager of the investment division at property consulting firm Colliers Halifax in Tokyo....

Read complete article here.

Analysts indicate property prices in Japan may be near bottom, Property Wire, Friday, 04 June 2010 .

I first put up this video on 13 March but I think it is worth watching again. A video interview with Marc Faber (Posted Mar 12, 2010 07:30am EST by Peter Gorenstein):

"If you are going to put money to work in stocks both market watchers think Japan is the place to be. After a 20 year bear market and despite high-debt-to-GDP levels, the pair think the market has become too cheap to ignore. Always a contrarian, Faber believes the lack of interest in Japanese stocks makes it one of the most compelling buys in the world. "

Related post:

Buy Japanese real estate.

Golden Agriculture: Uptrend.

Saturday, August 7, 2010

58.5c is a natural resistance turned support if we look at the candlesticks formed in the last three weeks.

The current uptrend support approximates the rising 20dMA and would be somewhere around 57.5c in the next session. Price could decline, break support at 58.5c and hit 57.5c in a whipsaw before rebounding.

Since the price hit a low of 48c in May, the MFI, OBV and RSI have been rising together with the rising price. So? Growing demand, continual accumulation and bouyant price movement. All good news for bulls. If this continues, price could push upwards to retest 62.5c. Could it overcome this resistance level?

Crude Palm Oil (CPO) has recovered strongly in a steep line upwards and is now at RM 2,661. This is not far from the double top which saw CPO at around RM 2,710. Golden Agriculture would benefit from higher CPO prices and the market knows this. If CPO price breaks RM 2,710, we could see Golden Agriculture's share price rally to a new high.

Tea with AK71: Philips Blu Ray.

Friday, August 6, 2010

On Sunday, I bought a Philips Blu Ray player for a good friend as a housewarming gift. I got it from Courts near HDB Hub in Toa Payoh. I bought it because it was such a good deal. Listen to this: usually $299, it was going for $239! Also, they threw in a free HDMI cable and 2 free Blu Ray titles!

I got my Sony Blu Ray player just weeks ago at Best Denki in Vivo City for $299 and I had to pay $99 for a HDMI cable! I also had to spend more money buying a few Blu Ray titles at MJ Multimedia to start me off. Fortunately, MJ was having a GSS offer at $70 for two titles but it would still come to a total of $299 + $99 + $70 = S$ 468 to get the same deal as offered by Philips in Courts! It's a $229 savings!

Now, here is the issue: the free Blu Ray titles must be collected from Philips HQ in Toa Payoh Lorong 1. They were not available in Courts. The posters in Courts showed Wolverine, UP and a couple of other titles. The salespeople told me that my friend has to bring along the receipt and his IC to choose the titles of his choice. I dutifully conveyed the message when I gave the player to my friend. This was on Sunday.

This evening, my friend went to Philips HQ and they told him that only Night at the Museum 2 and UP are available. Initially, I thought that the other titles were fully redeemed. My friend told me he was informed that only these two titles are available all along!!! This is a clear case of misrepresentation!!! I am so upset but my friend took it quite well and told me not to be angry. Grrr!!!

If anyone from Philips HQ in Singapore is reading this, you guys are lucky I was not with my friend when he went to collect the discs. I would have given you guys a piece of my mind!!!

Saizen REIT: Oversold.

Thursday, August 5, 2010

Saizen REIT has been stuck at 16c for weeks. Nothing is happening and it is just a waiting game now. However, it appears that most of the weaker holders have sold.

The Bollinger bands have narrowed and the MAs are all flattening with the exception of the long term 200dMA which is still rising. In fact, the 20d and 50d MAs have merged and flatlined at 16c. 16c could either become a very strong support or resistance in future. Looking at the MFI and the Stochastics, we see that this counter is very oversold. The OBV shows a stalemate between accumulation and distribution.

Taking a look at the weekly chart reveals that the longer term demand has been trending up. The MFI confirms this. Price has also overcome the descending 100wMA which was a strong resistance. At 16c, the unit price is sandwiched between the flat 20w and 50w MAs. Although Mr. Market does not care for what I think, it seems to me that the unit price of Saizen REIT could only go up from here. Let's wait for the results.

AIMS AMP Capital Industrial REIT: Dragoning.

The latest substantial shareholder of this REIT, Dragon Pacific Assets Limited, has increased its stake in the REIT again today. Its stake increased from 7.21 % To 11.39 % and it now owns 167,010,000 units.

I have not been able to find any information on Dragon Pacific Assets Limited and I am very curious as to its background. I am also very curious regarding the identities of the sellers. The same reason has been given for the buy up as before: Acquisition for investment purposes.

The REIT closed at 23c, the upper end of its range and with it going XD tomorrow, I would be very surprised if this long term resistance could be overcome. Then again, never say never.

Noble: Downtrend.

Wednesday, August 4, 2010

Noble has been in a downtrend since the middle of March. This downtrend is intact. With MFI forming lower highs, which suggests a lowering demand, and OBV dipping gradually, suggesting consistent distribution, the technical picture is rather negative. The MACD is in negative territory and has just completed a bearish crossover with the signal line. Momentum is negative and it is not improving.

The counter is nowhere near oversold and price could sink lower if there is no catalyst strong enough to turn market sentiments positive. Price is currently resting on immediate support at $1.66. Immediate resistance is at $1.70 as provided by the 20dMA and candlestick resistance.

Wednesday, 04 August 2010

CapitaMalls Asia: Low volume sell down.

Price reached a low of $2.09 before closing at $2.11 which is the top of a mini double bottom formation. If $2.11 breaks, we could see a retest of the base of the double bottom at $2.02. How likely is this?

Although price has moved down, volume has likewise reduced. A low volume pull back. Good news. Second opinion? The OBV has turned down but it did not plunge which means no massive distributrion. Again, good news.

However, chart watchers would see the sell signal on the MACD histogram. If this is confirmed in the next session, price is more likely than not going to move lower.

Blackstone is buying real estate in Japan.

I came across an article published by Bloomberg on 22 July, 2010, that Blackstone may buy Morgan Stanley's real estate assets in Japan. Here are some salient points:

Prices for Tokyo office buildings have fallen as much as 50 percent from their 2007 peak, according to an estimate by CB Richard Ellis Group Inc.’s Japan subsidiary. Blackstone’s first purchase in the country, after opening a Tokyo operation three years ago, may suggest prices are set to climb, said Takashi Ishizawa, a real estate analyst at Mizuho Securities Co.

“The news confirms my view that property prices in Japan have reached bottom,” Ishizawa said in a telephone interview in Tokyo. “Now is the time to invest.”

Japan’s nationwide average land prices dropped 8 percent in 2009 from a year ago, the second straight annual decline, the National Tax Agency said in a report earlier this month.

Related post:

Starhub: Testing support.

Tuesday, August 3, 2010

Technically, this counter looks a bit weak. $2.38 has been established as a strong resistance while $2.30 is a many times tested support. Volume was rather high today as price started at $2.38 and travelled all the way down to test the support at $2.30 before closing just 1c higher at $2.31. Could the rising 50d and 100d MAs lend support to $2.30 or would the support break?

The declining MFI suggests that demand has weakened while the declining MACD suggests that the shorter term MA is losing altitude. All in, a rather ominous picture for the bulls. Support at $2.30 is critical. If this support level holds as momentum oscillators decline, that is a sign of strength. If it were to break, $2.22 would be the immediate downside target.

Tuesday, 03 August 2010

AIMS AMP Capital Industrial REIT: New SS.

There is a new substantial shareholder for this REIT: Dragon Pacific Assets Limited.

No. of Shares held before the change: 38,985,000

No. of Shares which are subject of this notice: 66,693,000

No. of Shares held after the change: 105,678,000

As a percentage of issued share capital: 7.21%

Reason given: Acquisition for investment purposes.

Many are probably wondering who are the sellers as this is probably a married deal. The volume is really very high. Fundamentally, more substantial shareholders with a longer term investment horizon is good for the REIT. They would give a stronger floor to the unit price and, therefore, a firmer platform for possible future price appreciation.

Technically, the big sell down today at 22.5c sent the MFI crashing into the oversold region. The MFI has also formed a lower high. What we see now is a negative divergence with price which has moved up to test the long term resistance of 23c in recent sessions. 23c remains a formidable resistance.

OBV dropped a notch and the MACD seems ready to form a bearish crossover with the signal line. With XD date approaching in another 3 days, a pull back in the unit price of this REIT is probable. In such an instance, expect initial support at 22c and a stronger support at 21.5c, the midpoint of the trading range (20c to 23c). Good luck to fellow unitholders.

CapitaMalls Asia: Sell on news?

The market seems unimpressed with CapitaMalls Asia's results. Price tried moving higher, touched a high of $2.18 before declining to close unchanged at $2.16. The MACD is back in positive territory which suggests that we are once again seeing positive momentum in price movement.

Although the rising MFI suggests a strong demand, the OBV has turned flat in the last two sessions which suggests that neither accumulators nor distributors have the upper hand. Therefore, the lower volumes in the last two sessions as the price tried to move higher should be taken as a strong cautionary note.

Having said all these, it is worthwhile noting that price has closed above the 100dMA again even though it's a black candle day. If the 100dMA is confirmed as the new support, price could move higher.

Tuesday, 03 August 2010

Genting SP: Bearish engulfing candle.

Genting SP spots a bearish engulfing candle today. This is a big black candle that envelopes the entire candle of the previous day. This is extremely bearish as it indicates that price started the day higher but met with resistance and turned down to close lower than the previous day's low. That this was accompanied by high volume makes it more ominous. The bearish situation is backed up by a sell signal on the MACD histogram and the MACD has turned down towards the signal line.

However, even with the massive sell down today, the uptrend is still intact. Look at the support line I labelled "uptrend support 2". This uptrend approximates the position of the 20dMA. Could price bounce off this support in the next session or continue to decline to test the many times tested resistance turned support at $1.20? Although the MFI has turned down, the uptrend is intact. OBV has turned down which indicates some distribution took place today.

Golden Agriculture: Sell down,

In my post on Golden Agriculture yesterday, I said that "Although volume expanded today, a case could be made that we are seeing a negative divergence with price. Just keep this thought handy."

Golden Agriculture started the day at 60c to hit a high of 62c before retreating to close at 58.5c on high volume. This is where we find the downtrend resistance which was overcome yesterday.

OBV has turned down which confirms that distribution is taking place. However, the MFI is now higher than the previous high. This hints that demand continues to be strong and there are buyers waiting to collect at lower prices.

Could 58.5c now serve as support? It could but we need confirmation. A stronger support is at 55.5c, as provided by the 100dMA.

Related post:

Golden Agriculture: Downtrend broken.

China Hongxing: Resistance broken.

Monday, August 2, 2010

Against the odds, China Hongxing broke the resistance provided by the 200dMA at 16c. It touched a high of 17c before closing at 16.5c.

The sell signal on the MACD spotted in the last session is now negated as volume expanded today with the move up in price. MFI and RSI rose and stayed in the overbought region. OBV rose higher which suggests increased accumulation.

I look at the weekly chart for a glimpse of the longer term picture. The MFI, RSI and OBV are all rising. MFI and RSI are not overbought yet. The MACD is still rising but in negative territory and its distance from the signal line is increasing.

The bullish crossover with the signal line was completed five weeks ago. Being in negative territory, this could just be a rebound but a strong one. The increasing distance from the signal line is bullish but as the distance widens, bulls should turn cautious as the last four weeks have seen some big moves upwards.

The descending 100wMA is at 17.5c in the next session and this could be a formidable resistance.

Hyflux Water Trust: Privatisation.

I still have 5% of my original investment in HWT left, having divested the rest in stages for capital gains. I planned to keep this remaining investment as a no brainer passive income earner for the longer term as I bought these at 30c early last year and the DPU is about 5c per annum, giving me a yield of about 17%. This is not to be, it seems. Looking on the bright side, I will be getting back some money and booking a gain.

-->

Healthway Medical: Underlying strength.

The sell signal on the MACD in the last session was negated today. In fact, the MACD seems poised to do a bullish crossover with the signal line in positive territory.

The rising MFI shows unabating demand. OBV shows gradual accumulation. 18.5c has been established as immediate support.

The rising 50dMA seems to be on course to hit 18.5c soon. Could this push the price of Healthway Medical's shares up at the same time?

Volume has been declining as price settled into a tight range of 18.5c to 19.5c. There were two sessions in which volume spiked but price was unable to break past 19.5c. This shows that there are still sellers out there. However, with the OBV gradually higher, the sellers might be thinning as more accumulate shares in the company.

Technically, this counter is looking interesting. Could we see a breakout soon? In case of a breakout, we could see a retest of 21c, the high of 16 Jun.

Golden Agriculture: Downtrend broken.

With the white candle formed today, closing at 60c, the downtrend which started on 11 January is effectively broken.

The buy signal on the MACD histogram spotted in the last session has been confirmed. Momentum oscillators are still rising, forming higher lows which is good news for bulls. Although volume expanded today, a case could be made that we are seeing a negative divergence with price. Just keep this thought handy.

If the positive momentum keeps up, we could see the next resistance at 62.5c tested. Immediate support is provided by the flat 100dMA at 55.5c. Uptrend support coincides with the rising 200dMA.

Tea with AK71: Bought a new car!

Sunday, August 1, 2010

On 2 May, I blogged about how expensive it is to buy a new car now. I mentioned that I paid only $80k for my current car, a Mazda 6, almost five years ago and that for the same price I could only get a Mazda 2 hatchback, not even a Mazda 3, now! I said I would continue driving my fully paid Mazda 6 for another few years.

Yesterday, I blogged about my Mazda 6 being pillarised in a carpark and how I toyed with the idea of getting a new car. I decided to just keep driving my pillarised Mazda 6 after some thought. However, I still went online and looked at what's new at Mazda Motors just for fun. I was kind of attracted to the new Mazda 2 sedan which was just launched recently. Why not the hatchback? Cars, for me, must have a boot.

The boot allows me to hide my car washing stuff and it also acts as an extra large bumper if my car were hit in the back by some reckless driver. Also, people cannot see what I have in the boot and would not be tempted to break into my car. Might be a false sense of security but it gives me a peace of mind.

As I had nothing much to do today, I went down to Mazda's showroom to take a look at the Mazda 2 Sedan. Mazda is having a 90th Anniversary promotion and I was given a $12,000 discount. So, final price is $71k for a new Mazda 2 Sedan with leather seats and solar film. They also offered me $29k for my old Mazda 6, accepting all the dents and scratches.

I made phonecalls to my parents to get their opinions before test driving the car. As my previous cars ranged from 1.6 litres to 2.2 litres in capacity, my major worry about the Mazda 2 was the possible lack of power, being a 1.5 litres. Driving the car, I was impressed by how such a small engine could deliver so much punch. I am not an engineer and I won't go into details like DOHC and stuff. The information is available online, I'm sure. Anyway, as you have probably guessed from the title of this post, I bought it. Decision made within two hours or so.

A smaller car with a more fuel efficient engine is environmentally friendlier and is easier on the pocket as well. I will save on petrol, road tax and maintenance. The car will get a 3 years/100,000km warranty which is good. I have replaced quite a few parts under warranty for my previous cars before. I think it will not be any different with this car. Did I mention I was given $300 servicing vouchers as well?

The only downside is, of course, the much smaller size and this will take some getting used to. Then again, most of the time, I am just driving myself around. The backseat is usually for my briefcase, my gym bag and my Crumpler. So, this will be my first practical car for city driving.

I had hoped to drive my Mazda 6 for more than 5 years. It seems that is not to be. I hope to drive this new car for more than 5 years. Wish me luck.

Related posts:

Tea with AK71: Buying car now?

Tea with AK71: Pillarised.

SPH: A new high.

SPH hit a new high of $4.20 early in the morning of the last session and closed at $4.13, up three cents from the previous session. Volume almost quadrupled from the previous session and this has corrected the negative divergence I have blogged about recently.

The MACD is once again pulling away upwards from the signal line in positive territory. The MFI is rising after forming a higher low, suggesting that demand is healthy. OBV turned sharply upwards, indicating ongoing accumulation.

Immediate support is resistance turned support at $4.08. Immediate resistance is at $4.20, the new high.

Related post:

SPH: Rising on low volume.

Tea with AK71: Pillarised.

Saturday, July 31, 2010

What is "pillarised"? I would be surprised if such a word existed. It is just a word that happened to pop into my head as my car had a close encounter with a pillar in the carpark this afternoon in Burlington Square. That building has to have one of the most badly designed carparks in Singapore! One particular turn near the exit ramp was very tight. Anyway, that's where my car's passenger door got "pillarised". Sob.

I usually drive well and I have survived even the most claustrophobic of HDB carparks. So, this accident was a bit of a shock for me. Talking to a friend when I reached home, he suggested that my car is too big. Too big? It's a Mazda 6! Imagine if I were driving a Mazda CX-7! Although my car is turning five in less than two months, mechanically, it is still in good condition. Change my car? I admit that it is a tempting thought but it is probably not financially prudent to do so.

However, a customer recently told me that the COE price is probably going to increase month after month because less vehicles are being scrapped. This would mean that prices of cars would keep climbing. He said if anyone wants to buy a new car, it is now! Where is my chequebook?!

Then, talking to my mom after the "pillarising" experience, she suggested that I wait a couple of days and if I really want to get a new car, do it. My mom is basically being very rational and hinting to me not to be impulsive, I'm sure. Cool down and think clearly. I just damaged my car. Do I want to damage my chequeing account too?

I took a shower and felt a bit better. I went downstairs, washed my car and decided that I could live with the damage for another few years. Yes, you guessed it. I don't think I will fix the dent and scratches although my dad might insist that I do. Will see.

Usually, I could manage very tight turns but there were too many things on my mind today and I was kind of distracted. Like I commented in one of my posts lately, work has been stressful. So, what is it about work that is stressful? Workload stress, I can handle but stress due to certain transgressions by people, I don't handle very well. It is the latter that has been bothering me in the last few days. People trying to take advantage of people and people not playing by the rules.

Unfortunately, some of us have the thankless task of policing people. It is worse when we have a conscience! The task is not so distasteful if we were able to punish the transgressors, ensuring they would not do the same things again. It is when we are not able to do anything more than issuing warnings that it gets irksome. Imagine a toothless dog guarding a home. You get the idea.

If we keep doing the same things the same way, things will never change. So, what do we do? Make plans to change the way things are done or make plans to do different things. I know we might not have a choice sometimes but if we have a choice, we should remember that we have only one life to live and we owe it to ourselves to live it well.

LMIR: Selling pressure.

LMIR touched a low of 47.5c before closing at 48.5c, the immediate support identified previously. That this support was breached on high volume is somewhat ominous for the counter. Remember that this support is also where we find the 200dMA. Closing below this level would indicate a likely change in the longer term trend of the counter.

MFI has formed a lower high, suggesting decreased demand. OBV shows a clear trend of distribution since accumulation peaked on 27 July. MACD seems set to do a bearish crossover with the signal line as a red histogram appeared. Could we see more selling down? The possibility exists.

It would seem that I am not the only person disappointed with LMIR's latest set of numbers.

Related post:

LMIR: DPU reduced 20%.

AIMS AMP Capital Industrial REIT: Firm.

Friday, July 30, 2010

The MAs are all rising but we have a sell signal on the MACD histogram. So, prudence dictates against buying more units in the current time frame at the current price. The downside risk is quite real especially once the counter goes XD. Of course, volume could suddenly expand if a pension fund or some such investor decides to buy up in the next session at 23c but that's pure speculation and falls in the realm of HA, not TA.

Related post:

AIMS AMP Capital Industrial REIT: Steady performance.

Tea with AK71: Singapore is going strong.

Have you noticed how packed the malls are these days? The fastfood joints are packing in the crowd even on weeknights. Even the Econ Minimart near my place is crowded in the evenings. What's happening?

Singapore's economy is powering ahead and would probably take the number one spot as the country with the highest growth rate this year. It is all very impressive but one wonders how much longer this level of growth could continue for.

The feel good factor has affected everyone for sure and two articles in Yahoo! Singapore, placed side by side, show consumer confidence alive and kicking here.

Serangoon condo sells like hotcakes

By Angela Lim – July 29th, 2010

Units at The Scala, in five residential towers, are between 472 and 2,142 sg ft each and range from one to four-bedroom apartments. They were sold at a whopping average price of S$1,150 per sq ft (psf), setting a new benchmark price for the area.

Demand for the remaining 300 units of the 99-year leasehold project near Lorong Chuan MRT station was so strong that organisers had to resort to balloting to decide who entered the showflats first.

Read article here.

Mad rush for Apple’s iPhone 4

By Ewen Boey – July 30th, 2010

SingTel’s iPhone 4s were available at their store at Marina Bay Sands, while M1 and StarHub had their launches at Paragon and Plaza Singapura respectively.

The M1 queue at Paragon was by far the longest as it snaked around the basement of the shopping mall, while customers at Starhub’s Plaza Singapura had to register first before joining the queue.

Read article here.

Should we start thinking like a contrarian? There is a saying in Chinese which translates to say "in times of peace, think of the potential pitfalls". Enjoy the good times but stay cautious.

Genting SP: Inverted white hammer.

Thursday, July 29, 2010

Price touched a high of $1.29 before closing at $1.27, forming an inverted white hammer in the process. This suggests some weakness: the upmove lacks conviction. The unimpressive volume confirms this observation.

Although the OBV is still rising, suggesting continuing accumulation, there is some profit taking going on and a stalling demand. This stall in demand is confirmed by a flat MFI which is bordering on overbought.

Many are expecting Genting SP to report a set of sterling numbers but till then, could we see price softening somewhat to retest support provided by the rising 20dMA? There is a chance and that might be an opportunity for any bulls on Genting SP to accumulate.

Thursday, 29 July 2010

SPH: Rising on low volume.

Price broke out of the many times tested resistance of $4.08 today to close at $4.10. However, the relatively low volume suggests that the price rose due to a lack of sellers and not because of an abundance of buyers. So, it throws up the question of sustainability.

The fact that there is continuing accumulation is not in doubt. The rising OBV confirms this. The MFI has recaptured its uptrend support, it would seem, and this suggests a return of demand.

Lacklustre volume not withstanding, price could possibly rise further to retest $4.17 without a significant expansion in volume if selling pressure remains absent. Such a rise in price would, however, be very fragile.

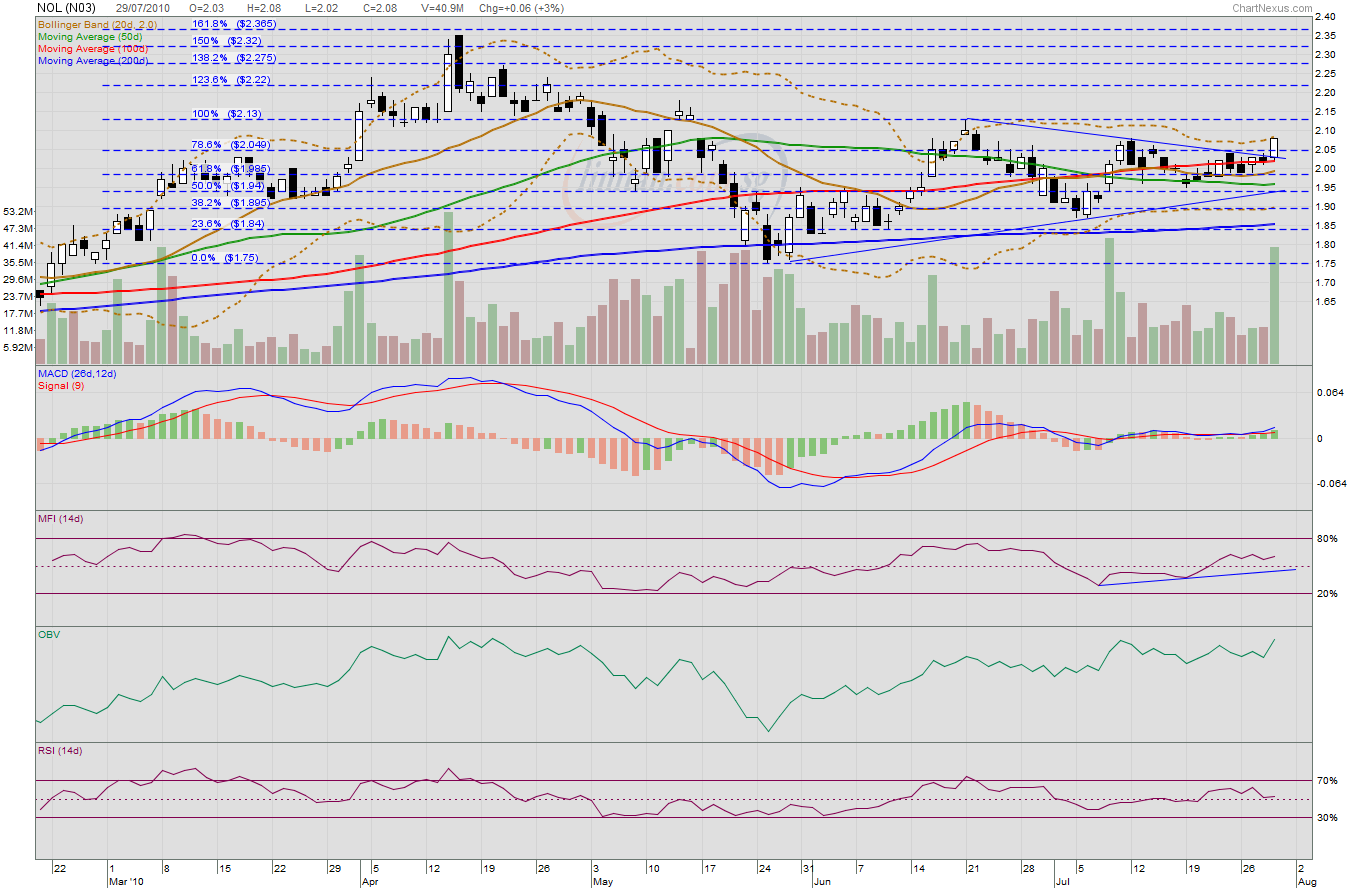

NOL: Breakout.

NOL rose to close at its high of the day at $2.08 on significantly higher volume. With this, it has broken out of the symmetrical triangle observed some time back. OBV has been somewhat choppy but rising further would indicate increased accumulation. MFI has formed an uptrend recently and this suggests increased demand.

The next resistance is at $2.13, the high of 21 Jun which also did a gap fill then. This is a price which market participants are likely to remember. Taking this out convincingly would give an intial target of $2.28 as suggested by the 138.2% Fibo line.

CapitaMalls Asia: Shopping spree planned.

"CapitaMalls Asia (CMAL.SI) could spend as much as S$3 billion to develop or buy shopping malls in Singapore, Malaysia and China, by using some borrowings on top of the S$1 billion cash that it has, partly from the proceeds of listing CapitaMalls Malaysia Trusts (CAMA.KL), the local press reported, quoting CapitaMalls' chief executive." Thursday, 29 July 2010, The Edge Singapore.

This bit of news sent the share price of CapitaMalls Asia up today to close at $2.10 which is the resistance provided by the flat 50dMA. The MACD has risen above the signal line in negative territory. MFI shows a sustained demand. OBV shows accumulation. Indeed, volume expanded more than three times over the previous session and is the highest since 12 Feb 2010. If the momentum continues, we could see price rising to retest the downtrend resistance which coincides with the declining 100dMA at about $2.16.

China Hongxing: Going higher?

China Hongxing breached 16c resistance and touched 16.5c briefly. Closing at 16c, it is still resisted by the declining 200dMA. This is a long term MA and unless volume expands significantly with any upmove, a breakout from the 200dMA is unlikely to be successful.

If we look at the volume, it has been declining as price tried to move higher in the last few sessions. Although not significantly so, it is nonetheless a negative divergence and calls for caution.

OBV is still rising strongly which means accumulation is still ongoing. MFI and RSI have both risen high into overbought territories. Momentum is still positive but the risk of a pull back is definitely higher now.

Taking some profits off the table would seem like a prudent thing to do and if price goes parabolic in the next session, I would divest more as parabolas are usually unsustainable.

Related post:

China Hongxing: Target hit.

LMIR: DPU reduced 20%.

LMIR announced a DPU of 1.04c payable on 27 August 2010. This is lower than the 1.2c paid in the last quarter. This is due to a higher realised loss on the foreign exchange forward contract. This reduced the funds available for distribution from S$13.9m in 2Q2009 to S$11.2m in 2Q2010. So, although the net property income increased 17.1% year on year, DPU has reduced 20% year on year from 1.3c to 1.04c!

I was under the impression that a foreign exchange forward contract is a hedge which would smooth out any currency fluctuations to help deliver a steady level of funds available for distribution, everything else remaining constant. It seems that I was mistaken.

The issue that bothers me now is that the management has no intention of reviewing its practice, it seems: "Despite the realised loss in the current quarter, the Trust has entered into the foreign exchange forward contracts as a prudent measure to mitigate its exposure to fluctuations of income denominated in the IDR". See press release here.

Therefore, I would hold off plans to increase exposure to LMIR on possible future price weakness.

Technically, LMIR has been on a uptrend since hitting a low of 42c on 25 May. A combination of its uptrend support and the candlestick supports shows immediate support to be at 48.5c in the next session.

Thursday, 29 July 2010

AIMS AMP Capital Industrial REIT: Steady performance.

Technically, price is still range bound and capped by the long term resistance of 23c. MFI has turned down and it remains to be seen if it could bounce off its support. 22.5c is now the immediate support.

What could go wrong?

Bremmer goes on to say that the markets have largely ignored South Korea's precarious situation. They should pay attention because Kim Jong-il wields enormous power and no one knows what he is capable of, including his presumed benefactors in China.

Genting SP: Doji.

Wednesday, July 28, 2010

Genting SP formed a doji today, a sign of indecision. Volume shrank today which is a sign that most people are staying sidelined. This stalemate is confirmed by the OBV which has gone flat. The MFI which has been rising and bordered on overbought has declined slightly.

Genting SP might just be taking a breather although with MFI almost overbought and RSI high in overbought territory, one wonders if it is ripe for a correction. Any pull back should see initial support at $1.20, a many times tested resistance level before and should be a strong support. This, incidentally, is also where we would find the rising 20dMA in the next session.

SPH: Retesting resistance.

SPH closed at $4.08 today, retesting the resistance identified some time back. This is the third time it has hit $4.08 since 16 July. Could it overcome this resistance soon?

Note the falling volume as price tried to move higher. The MFI has also broken down from its uptrend. Demand is flagging. OBV, however, is rising somewhat after a brief decline, suggesting renewed accumulation but the gradient is gentler now and one could even say it's flat as it is more or less the same level now as it was on 16 July. What am I trying to say? The technicals are relatively weaker now.

However, the 20dMA is still rising strongly and if price manages to stay above the 20dMA in the near term, SPH could be doing a correction using time and the 20dMA could push the price past $4.08 eventually. Keep an eye on the OBV. If it stays flat while the MFI declines, it would mean a lack of distribution and this might prevent price from sinking too much even as demand weakens.

Immediate support is at $3.98. This is where we find the rising 20dMA and it is also a natural candlestick support level. Good luck to fellow shareholders.

China Hongxing: Target hit.

On 24 June, I wrote "With momentum oscillators turning up strongly, we could possibly see 16c tested." Today, China Hongxing hit the breakout target of 16c. What next?

The OBV shows a sharp increase in accumulation. No distribution is taking place yet, it seems. However, MFI and RSI have both pushed into overbought territories. Also, notice the negative divergence between price and volume. A pull back in the near future is not unrealistic. Immediate support is at 14.5c followed by a stronger support at 13.5c. Remember, it's all about probabilities.

What would I do? I would lock in some gains. If I were to stay vested, it would be with a smaller position at this point in time. Congratulations to anyone who made money from this and if you see fit to contribute to my pocket money fund, thank you too. ;)

Related post:

China Hongxing: Breakout.

Mapletree Log: Acquires properties in Japan.

"MapletreeLog says it has sufficient financial flexibility and capacity to fund the Acquisition which is expected to be completed by end 3Q 2010. The purchase price and other acquisition costs of the properties will be fully funded by debt, which will bring MapletreeLog’s gearing level to 43.6%, after taking into account all acquisitions announced to date." (The Edge, 28 July 10, 13.23)

Its presentation slides show these acquisitions to be yield accretive. The investment would generate a return of 7.3% per annum. At the last traded price of 88c, the yield is currently about 6.8%. These Japanese properties are likely to bump up DPU by 5.6% per annum. The properties are also freehold in nature. No "depreciation". See presentation slides here.

Having said this, with these latest acquisitions, gearing level would be pushed up to 43.6%. One wonders if Mapletree Log would go to unitholders with hat in hand in the near future or, perhaps, do a share placement.

Wednesday, 28 July 2010

Alexa

I stumbled upon this today. I was totally blown away. This is a web information company and it has analyses of all the websites in the world. Well, it certainly looks that way to me.

I entered my blog's URL in the search bar and a one page analysis appeared. Amazing!

According to Alexa:

Singaporeanstocksinvestor.blogspot.com has a three-month global Alexa traffic rank of 667,393. Roughly 33% of visits to the site consist of only one pageview (i.e., are bounces). Visitors to the site spend approximately two minutes on each pageview and a total of ten minutes on the site during each visit. Visitors to the site view an average of 2.5 unique pages per day, and Singaporeanstocksinvestor.blogspot.com has been online for at least nine years.

I don't know about the rest of the information but my blog is not nine years old. So, perhaps, we should not take Alexa too seriously. Having said this, I am still amazed by this service. No wonder they say there are no secrets on the internet. We have to be careful of what we do in cyberspace!

Visit Alexa here.

A movie: The Last Airbender.

Monthly Popular Blog Posts

-

Hello everybody! This is AK. I am back! Time for another update. I talked about how I achieved financial nirvana in a YouTube video a few mo...

Hello everybody! This is AK. I am back! Time for another update. I talked about how I achieved financial nirvana in a YouTube video a few mo... -

People are naturally attracted by large numbers. I mean if we got a 5% discount off a purchase price, we might not be very impressed but...

People are naturally attracted by large numbers. I mean if we got a 5% discount off a purchase price, we might not be very impressed but... -

In the latest issue of The EDGE, there is a very good 2 page write up by Kelvin Tan on the current CPF rate debate. For anyone who would...

In the latest issue of The EDGE, there is a very good 2 page write up by Kelvin Tan on the current CPF rate debate. For anyone who would... -

I thought of not blogging about my 2Q 2020 passive income till a couple of weeks later because Mod 19 of Neverwinter, Avernus, just went liv...

-

Imagine a guy in Singapore who is in his 20s. Imagine he is in love with a female and they decide to get married right after graduation. Ima...

All time ASSI most popular!

-

A reader pointed me to a thread in HWZ Forum which discussed about my CPF savings being more than $800K. He wanted to clarify certain que...

A reader pointed me to a thread in HWZ Forum which discussed about my CPF savings being more than $800K. He wanted to clarify certain que... -

The plan was to blog about this together with my quarterly passive income report (4Q 2018) but I decided to take some time off from Neverwin...

-

Reader says... AK sifu.. Wah next year MA up to 57200... Excited siah.. Can top up again to get tax relief. Can I ask u if the i...

-

It has been a pretty long break since my last blog. I have also been spending a lot less time engaging readers both in my blog and on Face...

-

Ever since the CPFB introduced a colorful pie chart of our CPF savings a few years ago, I would look forward to mine every year like a teena...

Ever since the CPFB introduced a colorful pie chart of our CPF savings a few years ago, I would look forward to mine every year like a teena...

Bloggy Award

Bloggy Award