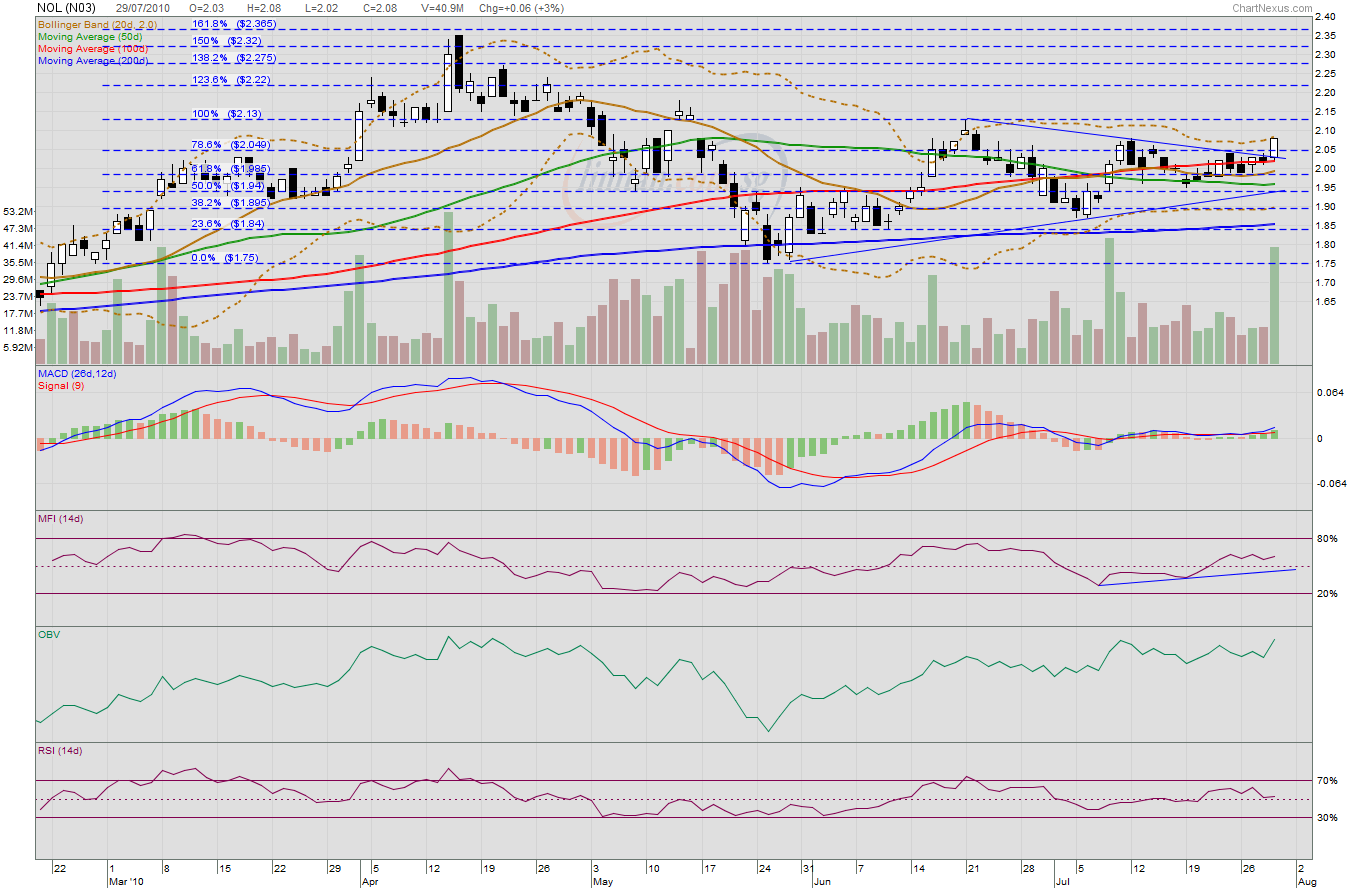

Genting SP: Broke resistance, gapped up and formed a wickless white candle on extremely high volume. Closing at $1.46, could it go higher next week? With such strong momentum and a flurry of BUY calls from all the research houses, we could see price going higher. To any investor who ignored the constant SELL calls from these houses earlier, congratulations!

Citigroup upgrades Genting Singapore (G13.SG) to Buy from Sell, lifts target price to $1.55 from $0.99 after increasing FY10-FY12 earnings estimates by 20%-80% to factor in robust 2Q10 results.

Friday, 13 August 2010

Friday, 13 August 2010

© 2010 - The Edge Singapore

China Hongxing: MFI has been declining gently, no longer in overbought territory. OBV rose today, sign of a return of accumulation activity. Volume expanded significantly as price rose today. This is promising. Closing at 15.5c shows that the declining 200dMA is still acting as resistance. Could the rising 20dMA push the price beyond the 200dMA? Immediate support at 14.5c and immediate resistance at 16c.

Hock Lian Seng: OBV shows a trend of consistent accumulation since 21 July. This company has strong fundamentals and, technically, the immediate support is at 28.5c, provided by the 100dMA. The rising 20dMA is on track to form a golden cross with the 100dMA soon. This would probably strengthen the support at 28.5c. Price seems to be forming steps upwards and this reminds me of HWT's chart once upon a time. The recent uptrend is defined by the rising 20dMA. Could the 20dMA push price higher? Possibly. Bugbear is the falling volume.

Hock Lian Seng Holdings, the civil engineer and a building materials supplier, says it posted a 61.9% y-o-y increase in net profit attributable to shareholders to $15.2 million in 1H2010 from $9.4 million in 1H2009.

Friday, 13 August 2010

Friday, 13 August 2010

© 2010 - The Edge Singapore

Bloggy Award

Bloggy Award